Learn why fintech APIs are driving an explosion of new business models, and how you can leverage APIs to power innovation.

Fintech APIs (application programming interfaces) are transforming an industry historically resistant to change. Their increasing adoption and use throughout the financial sector have resulted in an explosion of new apps, services and business models.

What Are Fintech APIs?

APIs allow different systems to talk to each other. In the context of financial technology—or fintech—they enable data access among the parties involved in financial transactions, including banks, third-party providers, websites and consumers.

Today’s most popular apps for checking the weather, finding flights and booking hotel rooms are fueled by the real-time data access enabled by APIs. But with traditional banking institutions maintaining a hold on customer data, API use was initially slower to catch on in the financial industry.

However, in the middle of the past decade, nations in Europe and Asia Pacific issued legislation that required banks to create and expose APIs, allowing third parties to access data with customer consent. The shift toward open banking spread quickly worldwide, resulting in a new generation of innovative and dynamic companies powered by fintech.

The increasing dominance of APIs in fintech is easy to understand. Banks and payment companies need to connect with third parties in order to expand their services and stay competitive. Merchants need to make it easy for customers to pay using their preferred methods and consumers want to be able to transfer funds, make purchases and perform personal banking tasks on the go. And for developers, APIs make creating financial apps and services faster, easier and more cost-effective than ever before.

Building Blocks for the New Fintech Era

The current success of many global tech leaders can be attributed to their strategic focus on IT services as a series of building blocks that are both interoperable and reusable. By providing apps and services for third parties to incorporate in platforms for their own customers, these companies grow their business and development ecosystems. APIs serve as the architectural components enabling this modular microservices strategy, and their adoption is evident in the rapid transformation occurring throughout the financial industry.

API use is driving innovation across industry sectors, including:

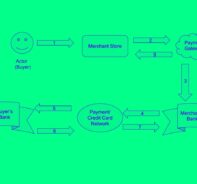

Payments and eCommerce: Connecting consumers, commercial websites and credit card companies, fintech APIs enable customers to make purchases and transfer funds through online platforms. Payment gateway APIs are a key focus for developers and marketers alike—they provide a seamless customer experience, allowing users to complete transactions without leaving a company’s website.

Banking: Banks are using fintech APIs to keep up with increasing consumer expectations for digital services and capabilities. A banking institution’s customer app is a common example—these platforms often connect with third-party APIs to provide services like credit score updates and mortgage tools along with standard account access.

Banking as a Service (BaaS): BaaS APIs provide third-party fintech companies with direct access to banking data. In this arrangement, a fintech pays to hook into an institution’s banking platform and create new offerings. For example, companies tie into banking APIs to deliver personal finance apps offering spending tracker functionality and investment recommendations.

Accounting: Fintech APIs also integrate accounting capabilities with other key business processes to improve efficiency. By connecting employee expense submissions with a company’s accounts payable function, for example, APIs eliminate time and resources spent on scanning, coding and entry tasks.

Financial Market Data: In an industry landscape previously dominated by on-premise data terminals, fintech APIs enable third parties to offer digital services that stream real-time financial and investment data from a vast range of sources.

The Pros and Cons of Using Fintech APIs

Before fintech APIs were widely in use, financial services and apps were typically costly and complex to develop. Simply connecting a platform with user bank accounts required development teams to build an integration for each financial institution involved.

Now, with players across the financial industry releasing their own APIs, you can easily integrate components to create a new offering or add capabilities. Using APIs as building blocks allows you to avoid recreating functionality that already exists, saving time and driving down costs.

Still, fintech APIs come with their own set of challenges. Some banking institutions have legacy systems that aren’t designed for smooth integration with APIs. Certain APIs were created quickly, under regulatory mandates lacking clear specifications or incentives to ensure optimal function and performance. And ongoing concerns about the potential for data breaches make secure connections paramount.

The Benefits of Fintech API Use Include:

- Faster solution development and accelerated time to market

- Significantly reduced development costs

- Reuse of components to eliminate unnecessary rework

- More time and resources to focus on innovation instead of repetitive development tasks

Potential Challenges Include:

- Legacy banking systems that aren’t yet optimal for API integration

- Rapidly launched APIs limited in function or performance

- Customer or partner concerns related to security

Which APIs Are Right for Me?

When choosing the best APIs for your organization, you may need to consider factors like use cases, customer needs and business strategy. In some instances, government regulations and compliance requirements come into play.

Most developers are in agreement, however, on the importance of certain overarching properties, including performance and ease of use. As a result, representational state transfer (REST) APIs have emerged as the leading style for web services development.

A true REST—or RESTful—API meets the following architectural criteria:

- Has a uniform interface for resources inside the system exposed to external API consumers

- Is client-server based (the client application and server application operate without dependency on each other)

- Is designed for stateless operations, in which the server doesn’t store anything associated with client requests—every request is treated as a new request

- Involves RESTful resource caching, which applies caching when resources have approved it

- Allows for the use of a layered system architecture

- Is designed for code on demand (optional), allowing a server to add more functionality to the REST client by sending code to be executed by that client

In contrast to more rigid API styles like Simple Object Access Protocol (SOAP), RESTful APIs offer optimal flexibility and usability for creating web services and applications. Almost every API within a web app is a REST API and, now, many cloud-based services provide a REST API for external users.

Our Core Suite of Fintech APIs Includes:

- Rapyd Collect. Accept hundreds of payment types—including credit and debit cards, bank transfers, ewallets and cash—from consumers in more than 100 countries. Using location data to automatically offer the payment methods your customers prefer, Rapyd Collect ensures that your checkout process always feels local.

- Rapyd Disburse. Start disbursing funds globally with the simple Rapid Disburse user interface and pay your partners and customers the way they want to get paid.

- Rapyd Wallet. Offer Raypd Wallet ewallet functionality under your own brand and empower your users with a personal financial hub for receiving, storing and sending funds.

- Rapyd Issuing. Issue cards and account numbers to ewallets with Rapyd Issue and offer your customers a powerful financial tool for use like any debit card.

Join the Conversation

Share your experience with payment APIs and join the Rapyd Developers Community.

Photo by Startup Stock on Pexel

Subscribe Via Email

Thank You!

You’ve Been Subscribed.