One of the biggest challenges for modern e-commerce and fintech developers is building checkout and payment processes that feel seamless, fast, and secure. But you also have to be aware of the user experience (UX).

Shopping online can often feel impersonal to the buyer as they’re ushered from one screen to the next. Along with security concerns, the impersonal nature of websites is one of the reasons many consumers are still reluctant to shop online. How can you address these concerns programmatically? What steps do you need to take to give users a more personalized payment experience?

One way to achieve this is by providing buyers with more payment options. But this does add an additional layer of complexity both programmatically and in terms of UX design. And how do you build an effective payment process with all these demands?

This article explores the essential design and performance considerations of building a marketplace payment processing system.

What Is Marketplace Payment Processing?

Marketplace payment processing describes the functions, procedures, and technologies involved in online transactions, typically in a multi-vendor platform. This includes payment acceptance from buyers, sending payouts 2 to the sellers, and possibly building a way to store funds on the platform.

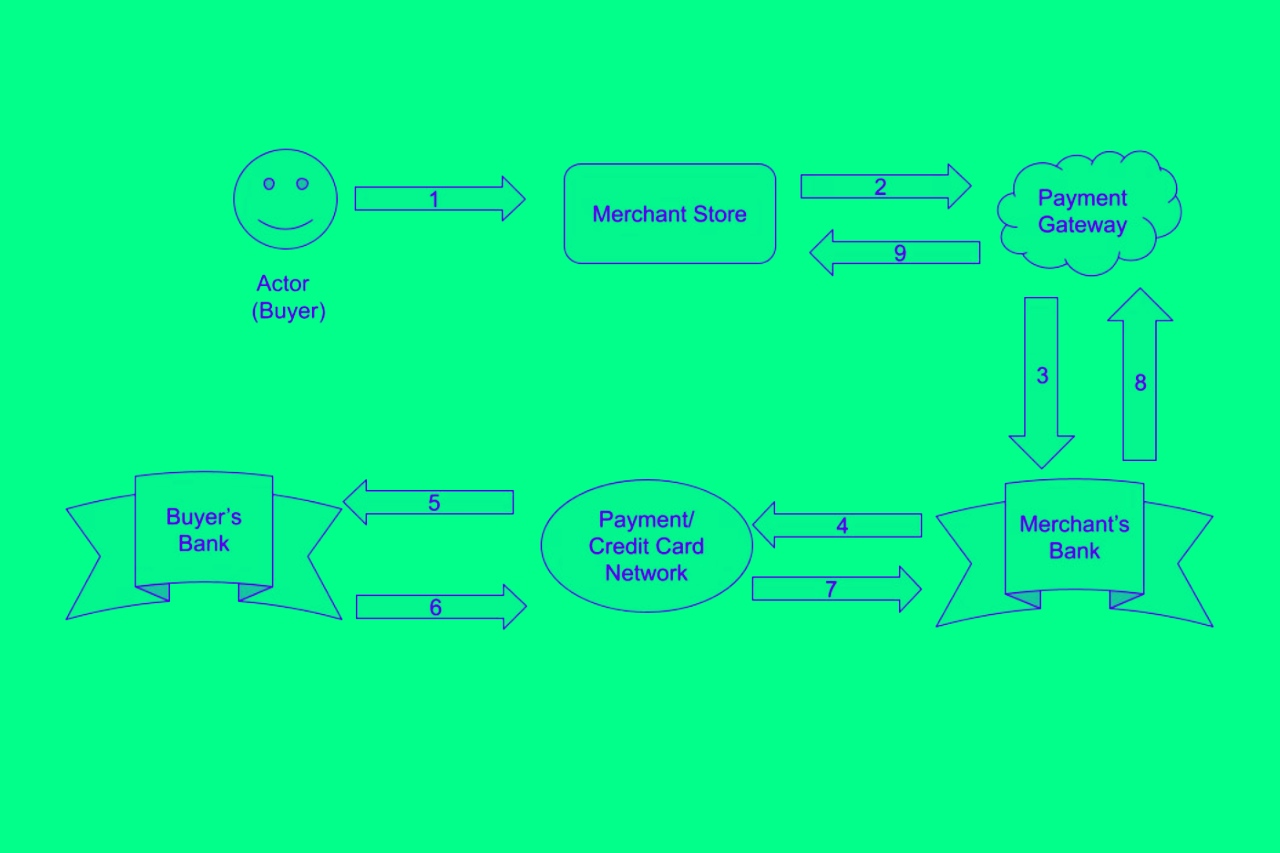

It seems simple enough, but it often involves multiple parties, especially for multi-vendor marketplaces. In addition to the buyer (card or account holder) and seller (merchant), other participants involved in traditional marketplace payment processing include the acquirer (merchant bank or service that processes payments), credit or debit card network or brand, and card issuing bank.

The participants involved may differ based on the type of transaction or payment being processed. For instance, cryptocurrency-based payments are still fairly new to being used in everyday marketplace transactions. As such, they aren’t likely to involve credit or debit card networks or issuer banks. However, they may be verified by transaction validators in the blockchain.

This highlights one significant challenge of modern marketplace payment processing. One of the biggest reasons customers abandon their carts at checkout is because the payment gateway doesn’t cater to their payment preferences.

If you want healthy conversion rates, your marketplace must provide potential customers with a diverse set of payment options.

Often, building this on your own can be quite complex. It requires you to build a scalable system that has multi-currency support and facilitates swift payment dispute resolutions.

Additionally, this system must be secure, provide ample user authentication, and perform optimally at all times. This means implementing performance monitoring tools and ensuring that you have adequate secure storage. But as you’ll see in the rest of the guide, this is just the tip of the iceberg.

The rest of the article explores the challenges and best practices associated with security and compliance and user experience (UX) and design when building a marketplace payment processing system.

Security and Compliance

If your global marketplace operates in multiple regions, it must comply with the specific personal data privacy regulations in each of those regions, such as the EU’s GDPR (General Data Protection Regulation) and Singapore’s PDPA (Personal Data Protection Act). Additionally, if your marketplace processes credit and debit card data, it is imperative to adhere to the Payment Card Industry Data Security Standard (PCI DSS). PCI DSS applies to any entity handling such payment data, ensuring its security.

While PCI DSS compliance should be a primary focus, it’s essential to recognize that some aspects of payment processing may fall outside its scope. For example, earlier versions of PCI DSS did not cover e-wallet transactions that didn’t involve primary account numbers (PANs). However, subsequent updates, like versions 3.2.1 and 4, have expanded the guidelines. This means that you should keep up-to-date with the latest standards in all regions where your business operates. The consequences of noncompliance, as evidenced by GDPR fines totaling over EUR 2.77 billion since 2018, can be financially debilitating, underscoring the importance of safeguarding both payment and personal data.

Employ Ample Encryption and Authentication

To ensure you’re providing adequate protection for data, you first need to cover the security basics. Most websites, including those with payment processing, use web encryption protocols such as Secure Sockets Layer (SSL) and Transport Layer Security (TLS) that ensure that data transmitted between your website (marketplace) and its users can’t be hijacked and spied on.

However, your online marketplace should employ this at large, not just for payment processing. Your payment gateway should also include end-to-end encryption (E2EE), which combines raw card data encryption, network tokenization, and payment data handler encryption. One of the best ways to implement E2EE is through JSON Web Encryption since it supports both symmetric and asymmetric encryption.

Employing strong customer authentication (SCA) is also a must. This entails requiring customers to have valid and verified user accounts before making a purchase. Moreover, your payment processing system must support multi-factor authentication (MFA), where two or more user verification methods are employed.

If you hope to legally operate in the European Economic Area (EEA), your system should implement 3D Secure to accept online credit card transactions. 3D Secure helps protect cardholders from fraudulent transactions by verifying credit/debit cards against three different domains when a transaction is initiated.

Meet Industry Security Standards

The goal is to secure customer data and payment information at all stages, which is essentially the initial step towards PCI DSS compliance. However, PCI DSS goes beyond securing transactions. To ensure compliance with PCI DSS standards, you can utilize their handy reference guide and the Report on Compliance Template.

The PCI DSS’s requirements can be condensed into six main points:

- Building and maintaining secure networks and systems

- Protecting card and account holder’s data

- Maintaining a vulnerability management program

- Implementing strong access control measures

- Regularly monitoring and testing networks

- Maintaining an information security policy

Adding comprehensive monitoring and fraud detection can be particularly tricky, considering that you have to do it while being fully data compliant. Moreover, these laws and regulations are frequently amended. As such, you’ll need to ensure that your fraud management and transaction tracking features are as frequently updated and conform accordingly.

Modern fraud management systems utilize machine learning and artificial intelligence to discern fraudulent transactions from genuine ones. They can potentially adjust to new rules and laws as they’re codified.

You also have to meet the specific data and payment security standards relevant to your industry. For example, if your marketplace deals with medical equipment, Protected Health Information, or health insurance provider payments, then adherence to the Health Insurance Portability and Accountability Act (HIPAA) is essential. If your marketplace offers credit or payment plans to consumers, compliance with the Financial Industry Regulatory Authority (FINRA) and the US Financial Crimes Enforcement Network’s (FinCEN) Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations are necessary.

You should also pay particular attention to KYC and AML rules if your business operates in high-risk countries (on the gray and black lists) where financial crimes may be common. Of course, you don’t have to handle your marketplace’s security on your own.

Rapyd Protect is a first-of-its-kind cross-border fraud management solution designed to encompass all payment methods and provide full global coverage. It utilizes a specialized rule engine along with AI to detect high-risk transactions.

You can fully integrate it into your payment gateway system and never have to worry about complicated regional rules. However, Rapyd doesn’t take all control out of your hands. It also allows you to configure custom rules, manually assess high-risk transactions, block and filter bank identification number (BIN) ranges, etc.

User Experience (UX) and Design Considerations

Payment gateways tend to be the most underdeveloped parts of the online shopping experience. Many gateways offer white-label API solutions and leave it up to the client to build their interface while integrating with the API. Many out-of-the-box solutions tend to aim for function over form. As such, they typically don’t follow the same design and themes of the marketplace user interface. The contrast can often be shocking, making payment gates feel less trustworthy. Thus, the same care and consideration you place on your marketplace’s UX should also be applied to your payment processing system.

Scalability and Reliability

Many developers fail to consider how critical scalability is in payment processing. For years, Blockchain technology (particularly) has struggled with bottlenecking due to scalability issues.

Ultimately, too many complex transactions occurring subsequently can slow networks down and prolong transaction processing periods.

Likewise, if your system isn’t equipped to handle sudden spikes, it may experience constant dips in performance or worse—complete outages. Customers and users want an online payment processing experience that is smooth and seamless.

Long processing times may cause or increase online purchase anxiety. Even if your system is secure, slow transaction processing speeds indicate that something may be wrong. Thus, making it feel unsafe. This can cost you long-term customers.

To prevent this, you need to employ a performance monitoring tool to identify any bottlenecks or performance dips. Most good modern payment orchestration platforms and solutions allow you to monitor transactions in real-time.

Of course, you can implement or build your own transaction monitoring tool. It should provide you with full holistic visibility – showing you all key metrics. This will make it easier for you to identify why a transaction has failed or why it’s taken so long to process.

Nevertheless, transactions aren’t the only elements of your payment processing system as a whole whose scalability you should consider. Your payment processing and eCommerce may suffer downtime due to maintenance and updates. You can minimize complete service blackouts during these periods by ensuring that your web components are properly encapsulated and using an efficient continuous deployment strategy.

In some cases, downtime and outages may not be related to system updates. Unforeseen and unplanned outages can occur due to power failures, hardware issues, internet disruptions, etc. In these situations, the goal is to maintain service continuity or at least the illusion of it. First, your payment processing solution should have a status page that anyone can access and review to check if your system is down. You should also communicate with site visitors, informing them that your gateway or one of its providers is down.

You can also deal with payment provider outages using routing and cascading. However, this will require you to have a diversified set of payment providers. When one payment provider fails, you can send the buyer to another.

Diversify Your Payment Options

Modern payment processing systems still follow some of the core principles of the traditional payment process flow.

However, because modern gateways offer several payment methods, they require more complicated flow designs. It’s best to design a separate flow diagram for each payment process.

You also need to take the areas you operate into consideration. Different districts and regions may have different rules and regulations that your system must conform to. With modern marketplaces operating cross-border, your payment processing system has to have multi-currency support.

Sometimes this means establishing partnerships and building networks with a variety of payment providers, banking institutions, and businesses. The simplest way around this is to partner with or integrate the services of an APAC treasury and trade solution.

Some providers offer multiple payment integrations. In addition to credit or debit cards, your marketplace should facilitate other transaction types, such as bank transfers, e-wallet payments, and cryptocurrency.

Of course, there are still countries with very limited internet connectivity and payment options. Thus, it’s important that the platform, provider or partner you choose offers cash options too.

Ensure Extensibility

In 2023, over 55.5 percent of all web traffic came from mobile devices. Despite personal computers producing higher conversion rates, it’s still very important to make an extensible marketplace payment processing system that can cater to as many internet-enabled devices as possible. If you’re creating a gateway and intend to use or supply it for third parties (not just your own marketplace), you must ensure that it delivers a consistent experience across devices and platforms.

Your payment processing system should be able to perform uniformly across all resolutions and screen sizes. This will require you to conduct thorough multiplatform unit and UI testing.

You can also allow third parties to integrate your gateway through APIs and other web integrations. Your marketplace or website isn’t the only one that may benefit from our payment processing system. You can produce more streams of revenue by allowing other developers and online storefronts to subscribe or purchase the rights to use some of your payment processing system’s functionality. You could limit this to the front end, enable access to your providers, or use your monitoring and verification systems. Alternatively, you can just package and encapsulate your code and reuse it for in-house purposes.

Focus on Customer Experience Management (CXM)

Whether your client is a buyer or a third-party merchant, you must ensure that they can easily get in touch with your business. This will require you to provide them with as many communication channels as possible.

Poor customer service and management is one area where many companies fall short. If you want to retain your clients and nurture good relationships with them, you must ensure that your company is as reachable as possible. You should employ friendly and well-trained support staff. Integrate automation where necessary but don’t rely on it too much as people prefer live agents over AI-based chatbots.

Being reachable allows you to resolve customer queries more swiftly. Your system needs to encourage customers to return. As such, your system needs to handle refunds and payment disputes.

Allow the customer/visitor to choose how they’d like to be refunded. Whether it’s through in-store credit, a voucher, digital wallet, the original payment method or Electronic Funds Transfer (EFT). Visitors should also be able to choose how they want to be refunded.

If a purchase or transaction fails due to an error on your side, you should consider adding a function that can automatically offer incentives to disgruntled customers. This can be in the form of discounts for their next purchases, free products/samples, vouchers, etc.

However, customer support is only one element of CXM. You also need to personalize your checkout and payment processing system accordingly. Language isn’t the only barrier when you’re operating cross-border. Different regions have different customs, cultures and tastes.

As such, your payment process needs to adapt to each region so it can deliver a culture-optimized experience. There are various tools you can use to extract consumer insights and trends. You can use Think with Google, Google Trends, Savanta, GlobalData, etc.

You can also develop your own customer experience surveys that you can either email as a part of your newsletters or they can be embedded on your website. It’s important to ask for feedback, conduct your own market research and look for ways you can improve your system.

Asking customers for feedback can also potentially increase engagement as it makes it feel like their opinions matter. It makes them feel important – and they are! This applies to B2B and B2C software vendors.

Ultimately, the most important part of CXM is delivering a good product. This means ensuring that your system not only works but also works well.

Do Not Neglect System Performance

Optimizing your payment processing involves minimizing waiting times in the payment flow to reduce purchase anxiety. Most online shoppers expect web pages to load in under three seconds. This applies to your payment processing system too.

Identify and address system bottlenecks that affect conversion rates. Additionally, as mentioned, you should set up a status page to alert and inform customers when your gateway experiences an outage. In addition to down detection, these status pages also offer a host of other functions to benchmark and monitor your web services and applications.

But how do you optimize your payment process if you find that it’s underperforming? Ensure your security features—like encryption methods—don’t hinder performance and address suboptimal code using linters and optimization tools. Reevaluate whether you need any code obfuscation techniques that might impact performance. Finally, you can also streamline UI elements, avoid excessive style sheets and scripts, and adhere to basic principles of web design to enhance overall system efficiency.

For deep performance tuning, consider specialized web applications and server optimization tools.

Conclusion

This article explored what it takes to make a great marketplace payment processing system, including some common pitfalls and how to overcome them. Security is still one of the biggest challenges. The goal is to find the right balance between security, user experience, and performance.

You can build your marketplace payment processing system from scratch, or you can use Rapyd, a global commerce-enabling platform that offers you a multitude of integration pathways. This includes a collection of global payment APIs, hosted checkouts, and virtual accounts. You don’t have to look over your shoulder and wonder when you’ll be fined for a breach. Rapyd is completely PCI DSS compliant.

Subscribe Via Email

Thank You!

You’ve Been Subscribed.