Here’s Your Easy-to-Understand Guide to Using and Implementing 3D Secure

3D Secure is an advanced authentication layer. It stops the unauthorized use of cards and protects and minimizes the fraud risk for eCommerce merchants and issuers. 3DS allows for card issuers and merchants to differentiate between good and bad transactions to mitigate fraud, while still allowing for transactions to happen instantaneously.

“3D” is short for “3 Domain”, which refers to the combination of the issuer domain, acquirer domain, and interoperability domain. Each card brand has its own unique version of a branded 3D Secure offering, with American Express Safekey®, Discover ProtectBuy®, Mastercard SecureCode®, and Visa Secure® as some of the most well-known offerings.

What is 3D Secure Authentication?

Do I Need to Use 3D Secure?

If your acquirer is located in the European Economic Area, you need to enable 3D Secure 2.0 to accept online credit cards – see map below. 3DS 2.0 is the easiest way to meet strong customer authentication (SCA) requirements for credit card transactions. 3D Secure requirements can vary by region but are well worth it to protect you and your business from fraud and chargebacks.

3D Secure is a method of authentication set up to protect you from incorrect or fraudulent online payments made by unauthorized cards. Created by Visa (‘Visa Secure’) and MasterCard (‘MasterCard SecureCode’), it adds an extra level of security and a bit of friction to the card payment process. 3D Secure 2.0 (also known as 3DS 2.0 or 3DS2) is the latest 3D Secure authentication protocol.

While 3D Secure is required to accept credit cards in Europe under Strong Customer Authentication regulation rules. 3DS is optional in other regions. Because it offers a liability shift that protects merchants from chargebacks from fraudulent transactions this makes it an attractive feature even for non-European merchants.

The 3DS2 Liability Shift is a Benefit of 3D Secure Transactions

Participating card issuers offer a payment guarantee for 3D Secure authenticated online payments. If a customer disputes a transaction for fraud, or claims that they did not make the transaction, then the merchant isn’t typically liable for the chargeback. The card issuer will pay those costs and the money won’t be taken out of the merchant’s account.

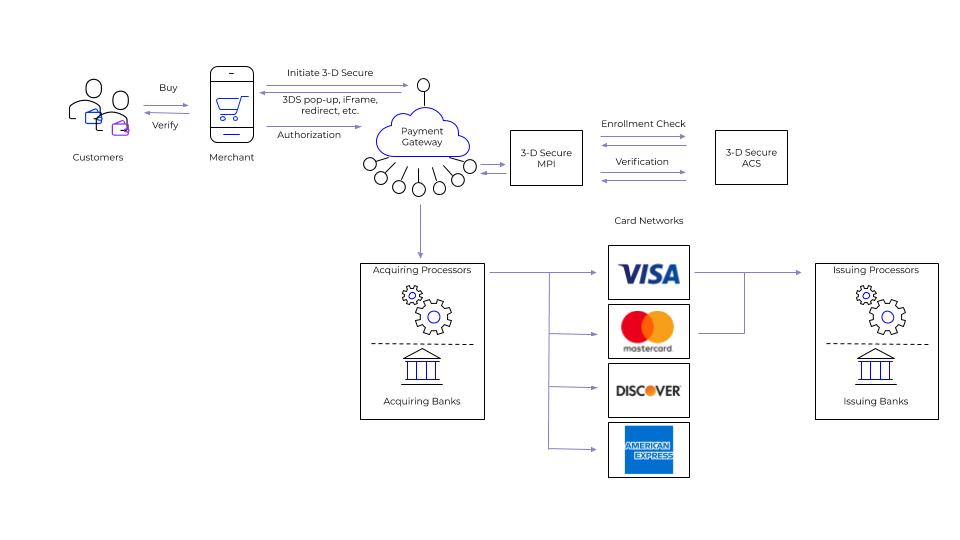

How Does 3DS Work?

The 3DS protocol allows merchants, card networks, and financial institutions to share information to authenticate transactions.

- Step 1: The customer inputs their card details at the checkout page or they are automatically scanned using a POS machine.

- Step 2: The customer’s bank evaluates the transaction and can finish 3D Secure at this step.

- Step 3: If their bank deems it necessary, the customer completes an additional authentication step, such as using a one-time authentication code, fingerprint or facial recognition.

- Step 4: Validated transactions are authorized.

What are the Benefits of 3D Secure 2.0?

By taking away the requirement for cardholders to manually enter a password, 3DS2 greatly lowered in cart abandonment rates. Now a detailed dataset related to the cardholder and the transaction allow for the issuer to make better decisions about whether the transaction is fraudulent. Cardholders also benefit from the sense of security of knowing that their card is not being misused.

With 3DS2 You Get:

- Better fraud prevention

- Mobile device support

- Multi-factor authentication and biometrics

- A better customer experience with fewer false positives

- More flexibility for merchants and opt-out capacities where not required by law

What’s the Difference Between 3DS 1.0 VS 2.0?

3DS 2.0 replaces 1.0. It offers a better user experience that helps to improve conversions and reduces cart abandonment.

With 3DS 1.0 customers had to enter a static password to validate transactions. 3DS 2.0 replaces these passwords with new authentication technologies, such as biometrics, to meet European strong customer authentication (SCA) requirements, analyzes over 100 data points, and asks users to verify high-risk transitions with biometric data or two-factor authorization

How Do I Set up 3D Secure?

In an ecommerce environment where cross-border purchases are only becoming more essential, you need to be able to verify card payments for your customers to mitigate risk and prevent fraud.

You can enable 3DS through a Payment Gateway or Processing Solution and Rapyd makes this easy. Check out How to Set up 3D Secure to learn how to request and complete a payment with 3DS for your customers using Rapyd. You shouldn’t have to take on any more liability and fraud risk than necessary. That’s why Rapyd supports 3D Secure 2.0 for Credit Card transactions.

Subscribe Via Email

Thank You!

You’ve Been Subscribed.