Here’s how a credit card payment processing framework can maximise your transaction approval rates

Credit card payments continue to grow. Retail and ecommerce volumes have already quadrupled over the past decade with digital card payments leading the charge.

This surge puts real pressure on your payment stack and can lead to low authorisations, false declines or drawn-out settlements. You need processing that keeps pace with rising volumes, tougher fraud tactics and evolving regulations.

This guide shares how credit card processing works and how to improve authorisation rates.

What Is Credit Card Payment Processing?

Credit card payment processing is the technological and financial infrastructure that facilitates merchants to accept card payments by supporting secure transaction authorisation, data transmission and fund settlement between multiple financial institutions.

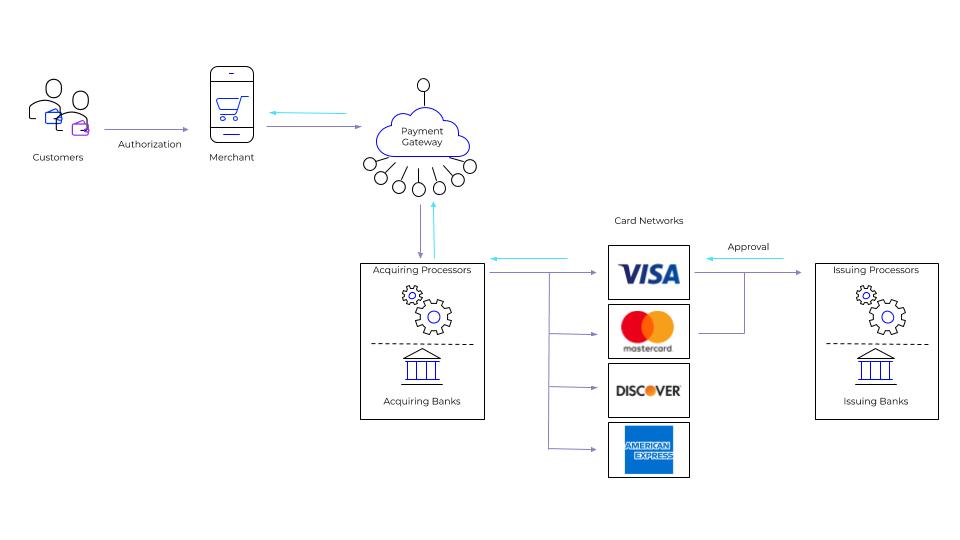

A successful transaction is a series of actions involving an entire ecosystem of participants. Each swipe, tap or online checkout is supported by:

- Card schemes that route data

- Issuing banks that approve or decline

- Acquiring banks that collect the money

- Processors that move the information between them

How Does Credit Card Payment Processing Work?

Because every participant takes a fee or sets rules, understanding how they interact helps you control costs, raise approval rates and stay compliant:

- Card schemes (networks): Visa, Mastercard, American Express and Discover run the global rails that carry payment messages. These networks set interchange fees and dispute rules, connecting acquirers with issuers. Visa and Mastercard operate open networks that allow any licensed bank to join while American Express remains a closed network that issues and acquires on its own rails.

- Issuing bank: This is the bank that gives a card to your customer. It decides whether to approve a payment after running fraud and credit checks. When a transaction clears, the issuer funds the acquirer and bills the cardholder. Cautious issuers can trigger false declines and lost revenue, so high authorisation rates depend partly on their risk models.

- Acquirer: It receives the authorisation request from your payment processor, forwards it through the network to the issuer then settles the funds back to your merchant account. The acquirer also shoulders fraud and chargeback risk which is why its contract terms cover rolling reserves and funding timelines.

- Payment processor: Processors provide infrastructure that moves transaction data between your checkout, the acquirer and the card networks. A reliable processor affects latency, uptime and reconciliation quality. All of these feed directly into customer experience and back-office efficiency.

- Payment gateway: In e-commerce, the gateway captures card details securely and tokenises sensitive data before passing it to the processor. By isolating your servers from card numbers, gateways reduce the scope of PCI DSS audits. Many gateways also connect to multiple processors, giving you redundancy without extra integrations.

- Payment service provider (PSP): A PSP, like Rapyd, bundles gateway, processing, acquiring services and even issuing into one solution. This one-stop approach simplifies onboarding and payments management.

What To Consider Before Accepting Credit Card Payments

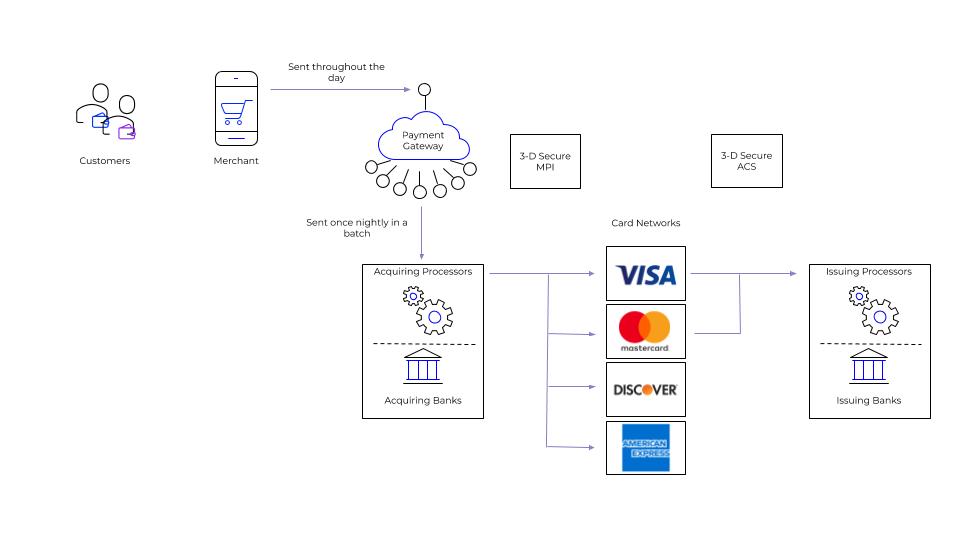

Understanding the transaction flow helps you spot bottlenecks, cut costs and hold processors accountable. The journey follows four connected stages—authorisation, capture, settlement and funding.

Credit Card Payment Authorisation

Authorisation is the critical yes/no checkpoint in the payment process. Your gateway sends card details to the acquirer. The card scheme routes them to the issuer. The issuer returns an approve or decline code.

Card networks now rely on 3-D Secure 2.0 for Strong Customer Authentication. This pushes a one-time challenge only when risk scores demand it. Parallel advances in tokenisation strip out the primary account number while fingerprints and face recognition replace typed passwords, reducing checkout friction.

Issuers may place an authorisation hold—often three to seven days—during which funds remain reserved but not captured. Direct acquiring relationships shorten this loop, increasing the chance your transactions clear on the first try.

Requests Capturing

Capture is your formal request to collect payment for goods or services. You can capture immediately after authorisation—common for digital content—or delay until goods ship. Delayed capture reduces refunds on out-of-stock items but extends the time funds stay in limbo.

Many merchants still batch capture at the end of the trading day. Yet digital wallets and click-to-pay checkouts favour real-time capture so customers see the final amount instantly.

Match your capture strategy with inventory cycles. For instance, a retailer shipping next-day can safely batch. A ride-hailing platform needs immediate capture to keep driver payouts accurate.

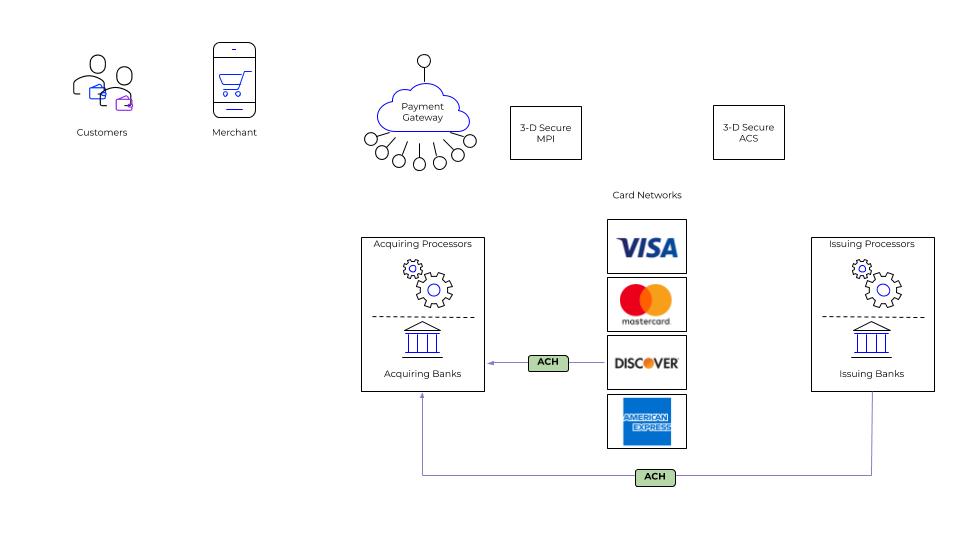

Settlement Timing

Settlement moves money between financial institutions rather than between you and the customer. After batched captures reach the acquirer, the card scheme nets credits and fees, then instructs issuers to transfer funds—traditionally an overnight process.

Demand for real-time payments is changing expectations, particularly in markets where instant banking rails already exist. Faster settlement cuts working-capital gaps and reconciliation windows..

Funding Timelines

Funding is when the acquirer deposits net proceeds into your business account. Timelines vary: low-risk merchants with solid volumes may receive funds one day after the transaction happens. Relationship strength, chargeback ratios and even weekday cut-off times all influence the clock.

Real-time settlement rails mean processors can now offer same-day payouts in many markets, a perk that supports tight cash-flow models such as on-demand delivery.

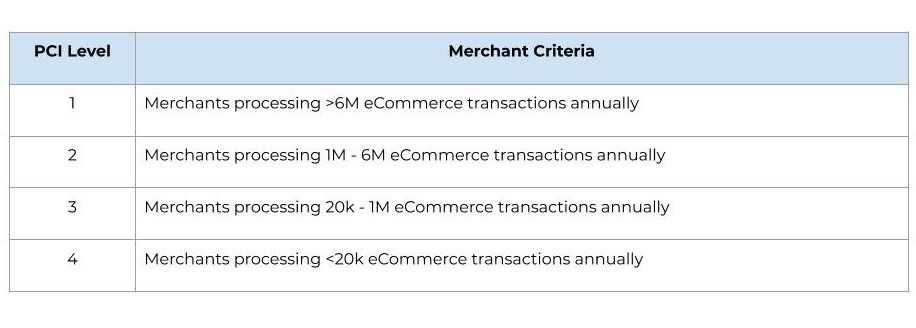

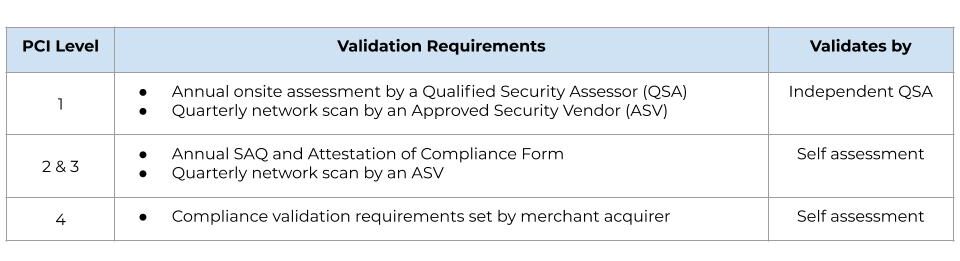

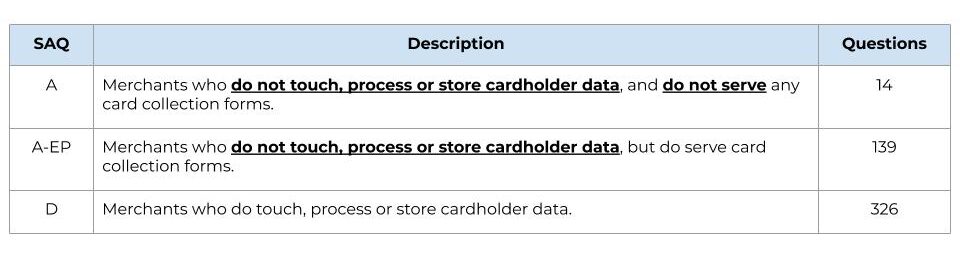

PCI Compliance

Every merchant that accepts credit cards is required to be PCI compliant. There are a number of factors that influence what is involved in achieving and maintaining compliance. Merchants are assigned a PCI Level based on their transaction volume.

This level determines their validation requirements:

Merchants must complete a Self Assessment Questionnaire based on the extent to which they handle, process and/or store cardholder data. This explains why hosted checkout is so valuable. If you don’t touch, process or store card data or serve any card collection forms, your scope and PCI responsibilities are significantly reduced.

Pricing and Processing Fees

Merchants pay the different parties for the services they provide during payment processing.

- The issuer gets paid by taking a percentage of each sale which is called the interchange and it can vary based on the industry, sale amount and type of card used

- The merchant bank charges a markup fee, based on the industry, amount of sale, monthly processing volume, etc.

- The credit card association (Visa, MasterCard, etc.) charges a fee, called an assessment

- The payment processor charges a fee for processing every transaction in addition to fees for setup, monthly usage or account cancellation

- Often these charges are combined into a single simplified price for merchants

Government Regulation

The Revised Payment Services Directive (PSD2) is a European regulation that governs electronic and non-cash payments.

It includes a mandate for payment service providers to implement strong customer authentication (SCA) for online payments and online banking transactions when both the issuing bank and acquiring bank/PSP are located in the European Economic Area.

3-D Secure 2.0 meets SCA requirements. For merchants who would like to avoid 3D Secure or another form of SCA for some transactions, there are a few exemptions:

- One leg out transactions: If either the Issuing Bank or Acquiring Bank/PSP is outside of the European Economic Area

- Low value: transactions under EUR 30

- Low risk/transaction risk analysis (TRA)

- Recurring transactions with the exact same amount

- Whitelisted merchants or trusted beneficiaries

- Secure corporate payments

How to Choose the Right Credit Card Payment Processor

Your processor choice directly impacts your revenue performance and operational complexity. The wrong partner creates false declines that cost you sales. The right one improves authorisation rates and simplifies your payment operations.

Make sure your process offers the following:

- High authorisation rates: Authorisation rates can vary significantly by processor. Rapyd provides some of the highest authorisation rates globally.

- Cards plus alternative payment methods: From ewallets to stablecoins, look for a processor who supports the methods that your customers trust.

- Built in fraud protection and dispute resolution: Simplify vendor management with an all in one solution that protects yoru business from fraud and chargebacks.

- Global reach: Choose a provider with direct local acquiring in the markets where you operate to maximise authorisations. Rapyd is a direct acquirer in the UK, EU, LATAM, Singapore and Israel with the ability to accept and send payments worldwide.

- Support for your sales channels: Do you need payments in store, online, in person or everywhere. Make sure your processor matches your needs.

- Easy integration: Whether your integrating via API, plugins or accepting payments with payment links and virtual terminals, make sure your provider offers the integration options you need backed by clear documentation and a robust support community.

3 Best Practices for Credit Card Processing Implementation Success

Successful credit card processing implementation requires careful planning and systematic execution. Your approach determines whether you maximise authorisation rates or create operational problems that persist for years.

Plan Your Implementation

Poor planning creates integration headaches. Rushed implementations often miss critical integration points, leading to reconciliation problems and customer experience issues.

Start with comprehensive integration planning before writing any code. Map your current payment flows and identify integration points with your existing systems. Your customer data, inventory management and accounting systems all need clean connections.

Then, create detailed testing phases that mirror your production environment. Test authorisation flows, decline handling, webhook processing and reconciliation procedures. Build error handling for network timeouts, gateway failures and unexpected response codes.

However, plan your rollout in phases. Start with a small percentage of transactions to validate performance. Monitor authorisation rates, settlement timing and customer experience metrics. Keep your rollback procedures ready until you confirm stable performance.

Optimise Credit Card Processing Performance

Declining authorisation rates often go unnoticed until revenue impact becomes severe. And problems are difficult to diagnose without proper monitoring systems.

You need to monitor your authorisation rates by card type, geography and transaction amount. Declining rates often signal technical issues or fraud rule problems. Track these metrics daily, not monthly.

Set up real-time alerts for authorisation rate drops, settlement delays or webhook failures. Payment issues compound quickly if you don’t catch them early. To avoid failure points, analyse your decline codes regularly.

Work with your processor to understand why specific transaction types get declined and how to improve approval rates.

Prepare for Growth and Peak Transaction Volumes

Capacity planning should happen before growth demands it. Transaction volume increases during promotions or seasonal events can overwhelm systems quickly. Test your limits and prepare scaling procedures to prevent payment failures during peak periods.

Subscribe Via Email

Thank You!

You’ve Been Subscribed.