Rapyd Disburse

GLOBAL PAYOUTS.

PERFECTED.

Rapyd Disburse is the cross-border payouts platform that makes sending funds around the world easier than ever.

DISBURSEMENTS FOR THE

WAY YOU DO BUSINESS

Single and Mass Payouts

Send payments to one beneficiary or hundreds. Online portal to easily track and manage all transactions.

Global Card Payouts

Push-to-card payments to credit or debit cards via Visa Direct and Mastercard Send. Access real-time payments 24/7.

Compliance Covered

Transaction monitoring, sanction screening and identity verification (KYC and KYB) to protect your business.

Stablecoin Payouts

Instant global transfers, constant 24/7/365 availability, and easy access to emerging markets.

Fill out the form and our team will be in touch fast.

Rapyd makes it simple to send payouts worldwide with bank transfers, real-time networks, instant card payouts and more.

CONTACT RAPYD

Support for Diverse Businesses

DISBURSE FUNDS.

DELIVER

CONFIDENCE.

With Rapyd Disburse you’ve got options. Our unrivaled network puts the best payout methods in one place.

Card Payouts

Send disbursements instantly to credit or debit card accounts in 190+ countries, 24/7/365.

Bank Transfers

Local clearing in more countries, including emerging markets. Lower costs while delivering funds quickly and securely.

Real-Time Payment Networks

Connect to real-time payment rails in more places worldwide and send funds instantly for less.

Third-Party eWallets

Use Rapyd Disburse to send payouts across Southeast Asia and Europe to popular eWallets.

BETTER FUNDS

MANAGEMENT

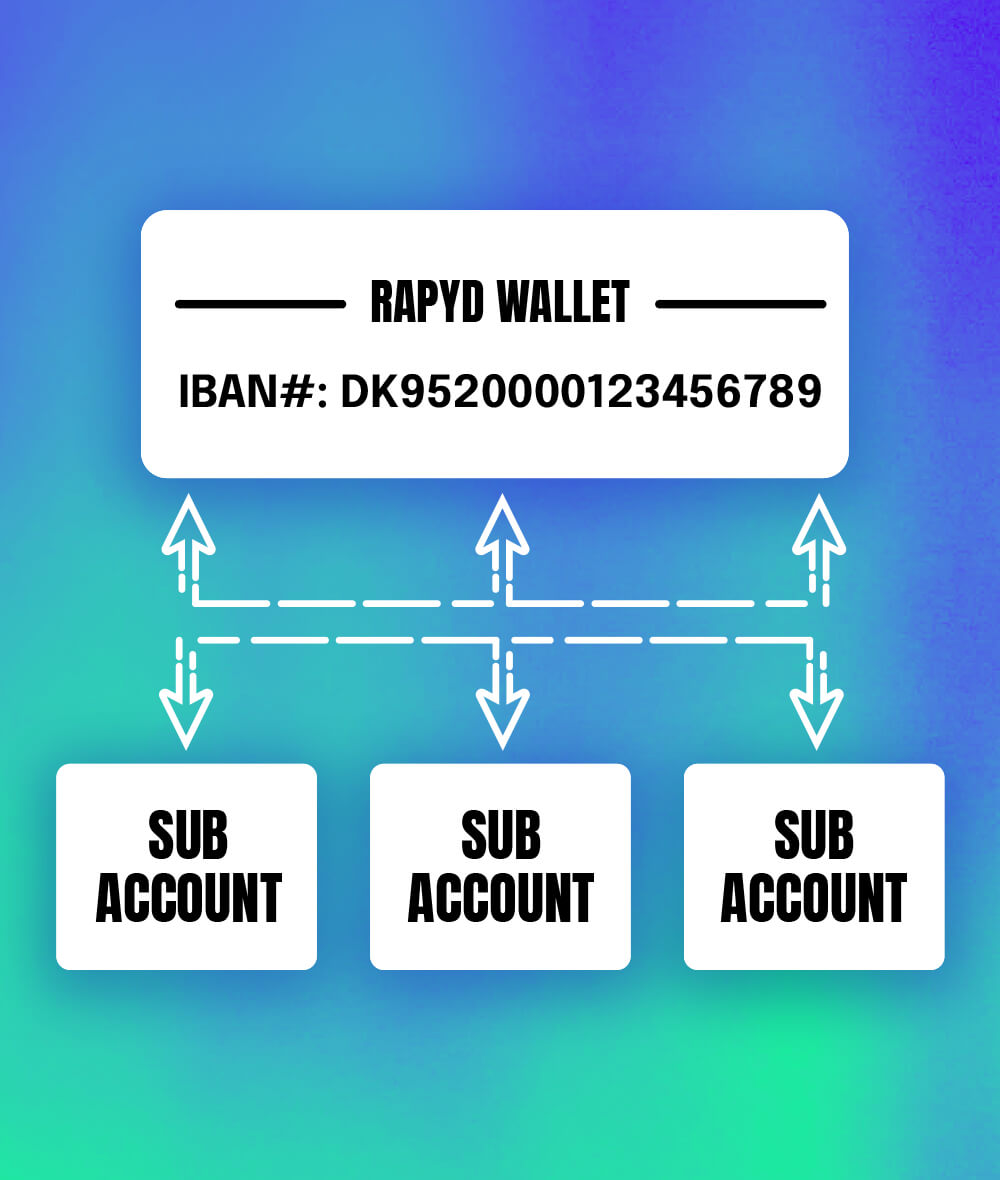

Monitor accounts, balances, events and financial transactions all in one place. Use Rapyd’s advanced account infrastructure to create accounts for your business and sub-accounts for clients, business partners or payees.

Rapyd helps SEAGM enter new markets quickly.

– Tommy Chieng, Co-founder and COO

By partnering with Rapyd, Kadmos clients experience a completely new way of paying their international workforce. Thanks to Virtual Accounts, it is faster, digital and much cheaper.

– Sasha Makarovych, Co-Founder

It is challenging to find partners to scale payouts across the Americas and Europe. Rapyd is making it happen.

– Ricardo Reis, Financial Operations

The Right Features for Frictionless Funds Disbursements

Foreign Exchange

Select disbursement currency and confirm exchange rates before sending.

Beneficiary Directory

Save user profiles and create pages for payees to enter their details.

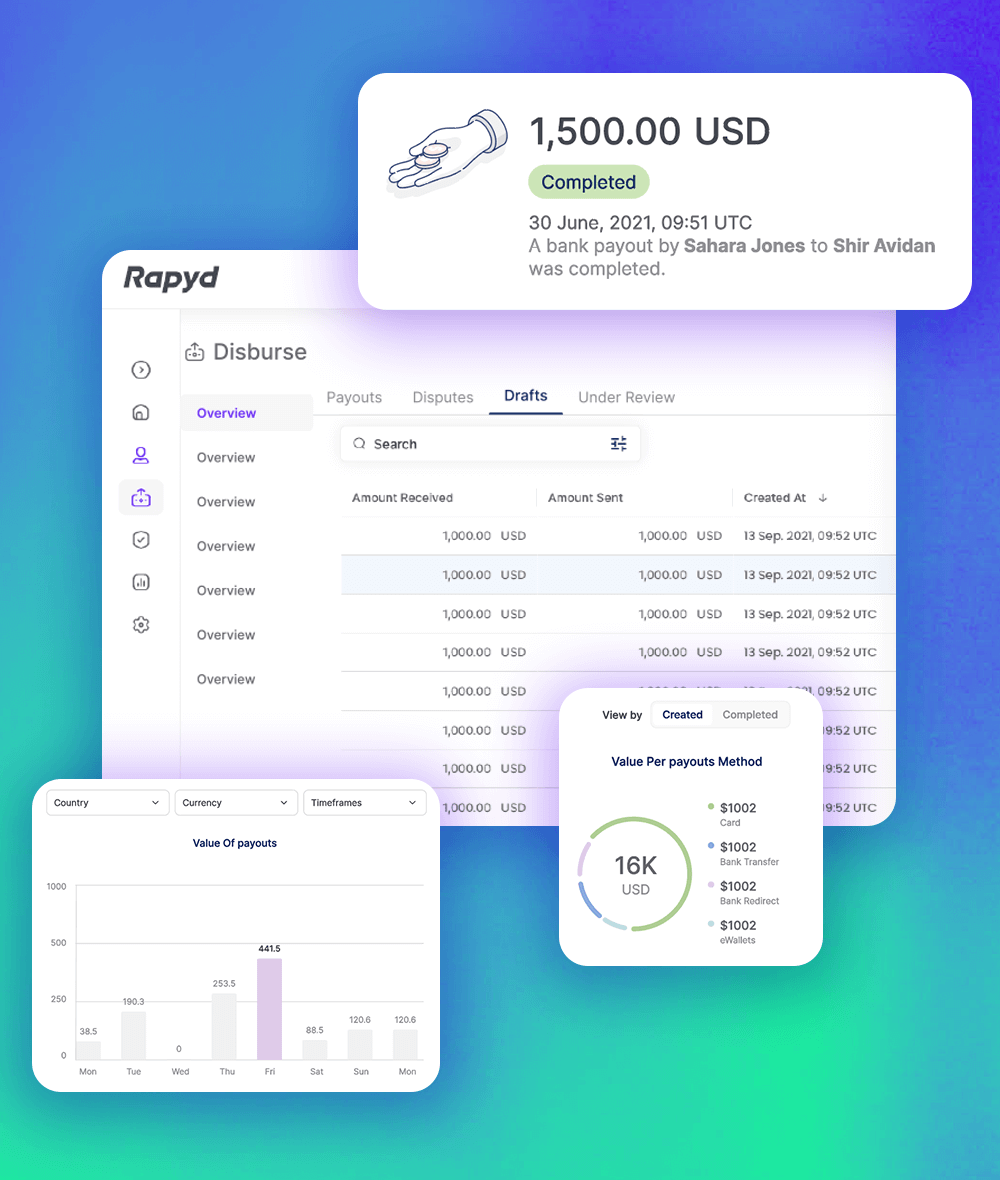

Modern Financial Ledger

Monitor accounts, balances, events, and financial transactions.

Powerful API

Use our API to integrate Disburse into your back office and bill pay applications.

Payout Tracker

Gain visibility into every payout, track status and set up notifications.

Virtual Accounts

Use Virtual Accounts to add funds that are available instantly for disbursement.

Rapyd Disburse Global Payout FAQs

Rapyd streamlines global payouts by replacing slow, manual wire transfers with a single, unified platform. Through one API or an easy-to-use portal, businesses can automate and manage cross-border payouts at scale—without relying on multiple legacy systems.

To accelerate payments, Rapyd supports:

- Card payouts via Visa Direct and Mastercard Send, enabling funds to reach recipients in minutes, 24/7

- Real-time payment (RTP) networks like Pix, Faster Payments, PayNow, and SEPA Instant, allowing transactions to settle in seconds

- Stablecoin-powered payouts give businesses and end users the speed, access, and stability they need—even in emerging markets—while helping you reach more customers globally, deliver instant payouts 24/7/365, and expand into new regions faster.

To ensure reliability and cost efficiency, Rapyd also offers:

- Smart routing and tracking to send payments via the fastest, most cost-effective path with full visibility

- Local clearing connections in 190+ countries for dependable, in-currency delivery

- Built-in FX to lock in rates and reduce exposure to currency fluctuations

- Virtual accounts (vIBANs) to simplify fund collection, prefunding, and global treasury management

By reducing payout times from days to minutes, Rapyd helps high-growth businesses improve cash flow, enhance payee satisfaction, and scale globally with confidence.

Rapyd is the best disbursement solution for complex use cases like iGaming, online gambling, forex and CFDs because it combines instant, global payouts (including stablecoins) with built‑in FX, robust compliance and reach into hard‑to‑access emerging markets through a single platform.

- Fast payouts that keep users in the game. Player loyalty depends on speed. Rapyd Disburse enables instant payouts so players stay engaged. Stablecoins are especially valuable for cross-border payouts, tournaments and promotions where speed directly impacts lifetime value.

- Stablecoins for 24/7 settlement and liquidity. Built into Rapyd’s core infrastructure, stablecoins offer 24/7, near-instant settlement without added complexity. Operators can streamline liquidity, reduce FX costs and settle in digital USD, then convert or disburse in local currencies as needed.

- Global reach, including hard-to-reach markets. Send payouts to 190+ countries using hundreds of local methods. Reduce friction, improve completion rates and scale faster.

- Built-in FX with 120+ currencies and stablecoins. A native FX engine lets you fund in one currency and pay out in another, with support for 120+ payout currencies and stablecoins—giving you flexibility to manage exposure and deliver funds in the formats your users prefer.

Rapyd Disburse is purpose‑built for complex, high‑volume disbursement flows, with support for one‑to‑one and mass payouts via API or portal, plus embedded fraud controls and compliance. That makes it a strong fit for industries like iGaming, online gambling, forex and CFDs that must manage strict KYC, AML and multi‑jurisdictional regulation while still delivering fast payouts to users worldwide.

Rapyd simplifies global mass payouts through a single API and unified wallet infrastructure.

Businesses can send thousands of payouts simultaneously across 190+ countries and 120+ currencies, using local rails, RTP networks, stablecoins or card payouts. Virtual accounts (vIBANs) enable seamless prefunding and treasury management without opening multiple local bank accounts.

CTOs and product teams reduce integration complexity, accelerate time to market, and scale payout operations without operational bottlenecks.

Yes, Rapyd’s Global Payouts infrastructure is built for scale, allowing Online Marketplaces and Content Creator Platforms to simplify single or mass payouts. By utilising our Virtual Accounts and Modern Financial Ledger, platforms can manage complex fund flows between buyers and sellers. This simplifies multi-currency management and ensures creators receive funds, even in emerging markets.

Rapyd’s global payouts via stablecoins and cards offer instant or near‑instant transfers and “always‑on” availability, even on weekends and holidays. By leveraging Visa Direct and Mastercard Send, businesses can push funds directly to a user’s existing cards, so recipients don’t need to open new accounts or wallets to get paid.

Stablecoin payouts let businesses send funds with lower fees and reduce prefunding requirements by bypassing many intermediary banks, unpredictable charges and slow delivery times associated with legacy cross‑border networks like SWIFT. Because stablecoins combine dollar liquidity with digitally‑native flexibility, they are a preferred payout option for many recipients worldwide who want the stability of a dollar‑linked asset without the friction of traditional bank transfers.