Rise of Super Apps: The Next Wave Will Be Led by Innovators Who Integrate Fintech into Applications

Marketplaces, social media apps, and gig-economy platforms in Asia are adding fintech to their offerings to create new sources of revenue and take seller, worker and consumer loyalty to new heights. By combining multiple functions like ride-hailing, ecommerce and food delivery with financial services, Asian tech giants have created a new app model that’s delivering frictionless user-experiences tailored for mobile-first consumers.

Businesses around the world are starting to take notice. Here’s what marketplaces and gig-economy platforms need to know to make your apps super too.

What Makes an App “Super”?

Super apps bundle multiple functions into one user experience and create a portal to a wholly-owned online ecosystem that includes a range of daily services, with payments at the core.

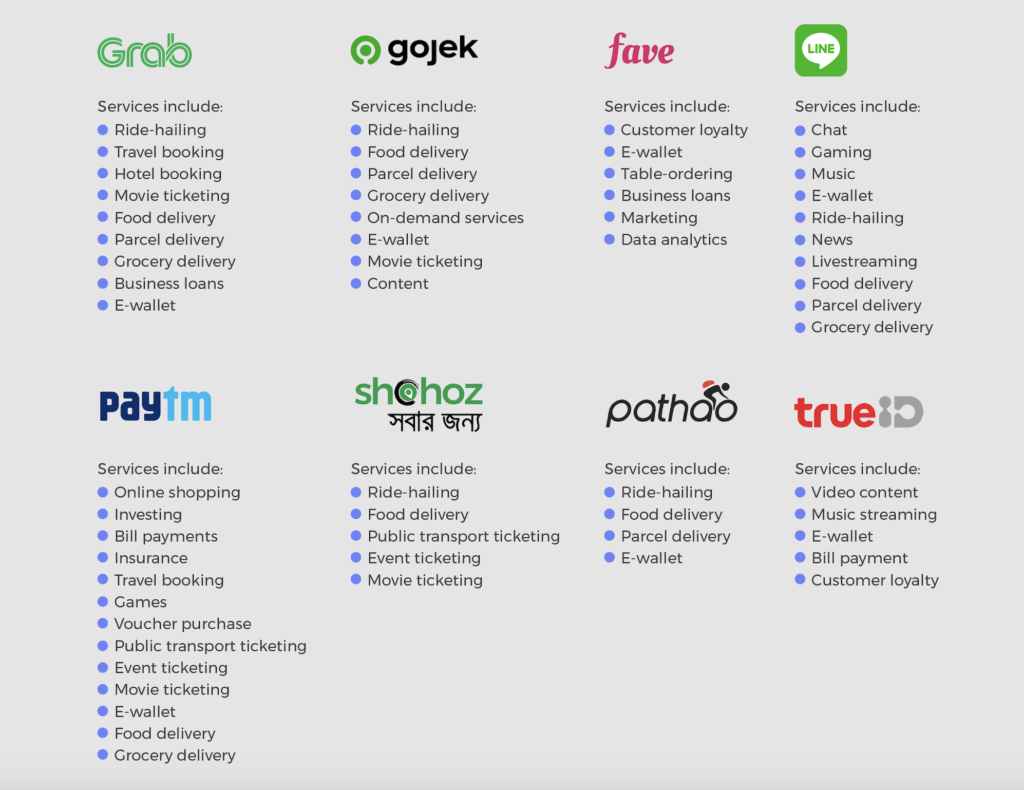

Notable Super Apps Across Asia

Why Super Apps Are Taking Off Now

One big reason is convenience. Super apps save space on smartphones and require fewer downloads and updates while removing the need to switch between apps.

Another key factor is the economic environment. In Southeast Asia, a combination of a growing middle class and high mobile phone penetration creates the perfect market for super apps to fuel super growth.

Southeast Asia’s middle class is projected to surge from 190 million in 2012 to over 350 million in 2022, and mobile broadband connectivity is 101%, reflecting individuals who own multiple connected devices1.

Where Will Super Apps Take Off Next?

The first generation of super apps, such as Baidu and WeChat came out of China about 10 years ago, and the economic environment in Southeast Asia now mirrors China’s environment then.

Countries in Latin America and India are also starting to look similar and may present fresh opportunities for super app innovation and expansion. Even developed nations in North America and Europe could also follow as wallets and card-not-present payments continue to gain in popularity.

How to Make Bank with Your Super App Strategy

In addition to multiple services such as ride-hailing, food delivery, social media, and ecommerce, what really makes an app “super” is providing payment, credit, and rewards features. “Once you’re handling money for a user, you can build a castle of services,” explains Sidu Ponnappa, Senior Vice President of Engineering at Gojek, Indonesia’s leading super app.

5 Ways Super Apps Power Revenue Growth

- Introduce and monetize credit to consumers, agents, and merchants.

- Offer cross-border payment capabilities for consumers and businesses.

- Earn fees and commissions from transactions on your marketplaces and platforms.

- Grow advertising capabilities to charge for ads and traffic to merchants.

- Use rewards to grow loyalty and transaction frequency.

Ready to Give It a Try?

- Provide a marketplace or gig-economy platform that uses localized payment methods to capture market share of both suppliers and consumers.

- Engage sellers, contractors, and users by leveraging ewallets to create frictionless commerce experiences.

- Engage agents, sellers, and users by adding incentives and rewards features.

- Continue enhancing the service by adding pay-later or credit capabilities as well as issuing virtual and physical cards.

Don’t Go It Alone

“To meet the scale of our ambitions, we collaborate with partners who are the best in what they do, combining their expertise with ours,” explains Jerald Singh, Group Head of Product and Design, Grab, Speaking to Tech in Asia.

Sources:

SCSME Bain & Company, Quartz. The ASEAN Post. We Are Social

Subscribe Via Email

Thank You!

You’ve Been Subscribed.