Explore the Rapyd Payment Network

When It Comes to Global Payments,

Connections Count

Liberate global commerce with Rapyd card acquiring, local payment methods and worldwide payout capabilities.

EVERY COUNTRY.

EVERY METHOD.

One integration unlocks local payment and payout methods across 182 markets.

Pick a region or search a country to see exactly what's available.

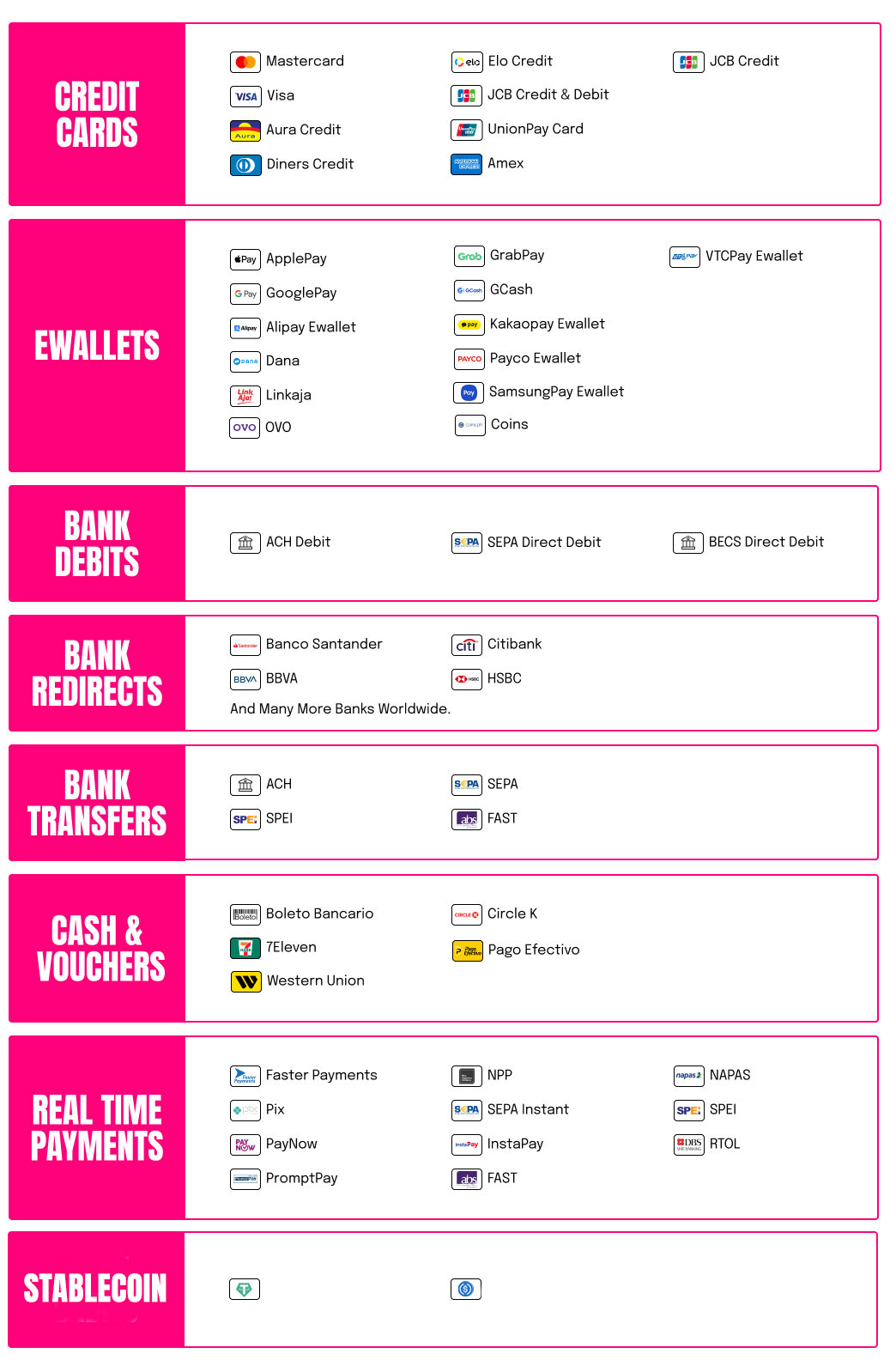

What Payment Methods

Can I Accept with Rapyd?

Accept hundreds of local payment methods worldwide with Rapyd, including credit/debit cards, Apple Pay, Google Pay, bank transfers, stablecoins, eWallets and cash. Contact Us for full details.

ANSWERS. GET THEM HERE.

Rapyd works with businesses that have legal entities in one or more of the countries below. If you are in one of these countries, contact us.

| Albania | Greenland | Philippines |

| Andorra | Hong Kong | Poland |

| Armenia | Hungary | Portugal |

| Australia | Iceland | Romania |

| Austria | Indonesia | San Marino |

| Belgium | Ireland | Serbia |

| Bosnia and Herzegovina | Isle of Man | Singapore |

| Brazil | Israel | Slovakia |

| Bulgaria | Italy | Slovenia |

| Japan | South Africa | Channel Islands |

| Latvia | South Korea | Colombia |

| Liechtenstein | Spain | Croatia |

| Lithuania | Sweden | Cyprus |

| Luxembourg | Switzerland | Czech Republic |

| Malaysia | Taiwan | Denmark |

| Malta | Thailand | Estonia |

| Mexico | Turkey | Faeroe Islands |

| Moldova | Ukraine | Finland |

| Monaco | United Kingdom | France |

| Montenegro | United States | Georgia |

| Netherlands | Vietnam | Germany |

| New Zealand | Virgin Islands | Gibraltar |

| North Macedonia | Greece | |

| Norway |

Rapyd partners with multiple technology companies and platforms to make accepting international payments easy. Some third-party companies have their own limitations for which countries they allow customers to be located in. They may also limit the number of locations you can accept payments from. Check out your plugin’s page in our docs to view supported countries.

Alternative Payment Methods (APMs) are local payment solutions such as digital wallets, bank transfers, mobile payments and cash vouchers for digital transactions. While credit cards remain popular, Rapyd enables businesses to accept both credit cards and a wide range of alternative online payment methods, providing a comprehensive payment solution for customers worldwide.

Accepting global payment methods, including APMs, is essential for businesses looking to increase trust and drive conversions. APMs cater to customers’ local preferences and have been shown to reduce cart abandonment rates – Offering preferred payment methods can improve conversion rates by as much as 30%.

Learn more about alternative payment methods and accepting cash for digital transactions.

With Rapyd, your business can simplify payment acceptance and optimise for global success.