Transform disconnected payment channels into a unified omnichannel payment infrastructure that maximises conversion rates

Imagine reviewing last quarter’s numbers and spotting an uncomfortable pattern: customers start checkout on your website, switch to a mobile app for a discount code, then walk into a branch to finish the purchase—only to abandon the sale because the card on file won’t transfer between channels.

The gap comes from a fragmented payment infrastructure, not consumer demand. When your channels don’t share payment data in real time, convenience turns into friction and revenue disappears.

In this article, we explore how to fix that through omnichannel payments.

What Are Omnichannel Payments?

Omnichannel payments are unified payment infrastructures that integrate multiple payment methods across all customer touchpoints while maintaining a consistent user experience and shared transaction data.

When every card swipe, wallet tap or pay-by-link runs through the same back-end, you see one customer, not scattered, disconnected transactions.

Why should you care? You should because fragmented payment stacks cost you money. Shoppers abandon carts when they can’t use the same payment method on mobile and in-store. Finance teams waste hours matching data across different payment gateways.

Unlike basic card processing, omnichannel payments platforms sync data in real time. A token created online follows the customer into your store. You can recognise their card instantly and approve refunds on the spot.

This continuous context simply isn’t possible when separate providers handle each channel.

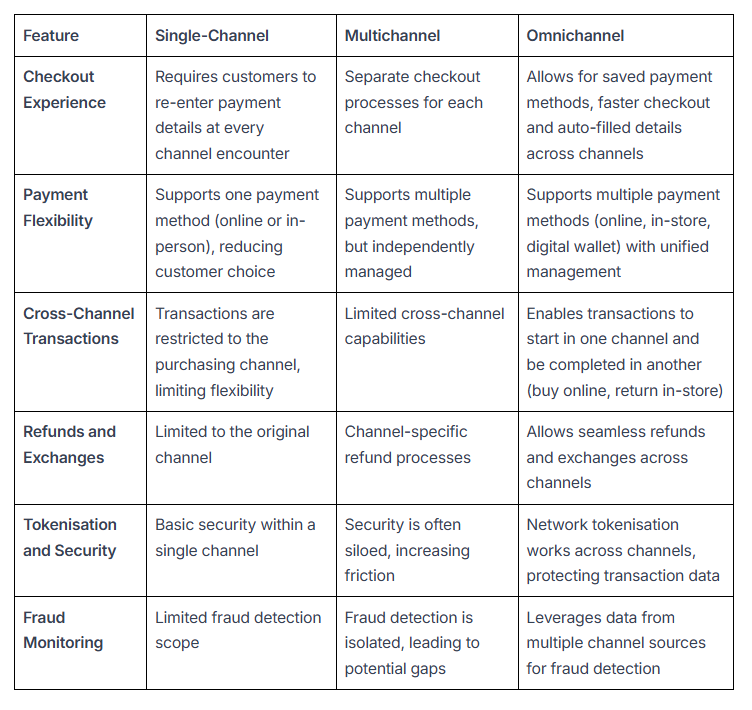

Single-Channel vs. Multichannel vs. Omnichannel

Let’s compare this model with older approaches:

Single-channel setups work fine for a kiosk or tiny merchant, but fall short when you add more sales channels. Multichannel improves reach, but each channel still operates independently. Data must be stitched together afterward and customers repeat steps when switching devices.

Unified omnichannel systems remove these barriers. You maintain one integration, one risk profile and one dataset. Shoppers move smoothly from digital ad to checkout to in-store pickup without friction.

How Does Omnichannel Payment Processing Work?

Understanding how omnichannel payment processing works explains why this approach beats scattered approaches:

- Integration across all channels: Connect web stores, mobile apps and physical terminals to the same gateway through APIs. This single point handles token generation, encryption and routing for all transaction types.

- Customer interaction & payment: Whether someone taps a card reader or confirms a wallet in-app, the request travels through the unified gateway to banks and payment networks. Fraud checks apply consistently, using the complete customer profile rather than fragmented data.

- Data synchronisation: Authorisation responses update inventory, loyalty and finance systems instantly. This real-time data flow means a basket started online can appear on the cashier’s screen moments later.

- Post-purchase experience: Tokens enable quick refunds, cross-channel returns and saved payment methods for future visits. Central dashboards track every transaction for reporting, making reconciliation much easier.

Benefits of Omnichannel Payments

For payment operations leaders focused on growth, the advantages are concrete. A comprehensive strategy delivers measurable improvements across key metrics:

- Higher conversion rates: Unified customer experience reduces cart abandonment and increases transaction completion across all channels

- Improved authorisation rates: Comprehensive customer profiles enable better fraud detection without blocking legitimate transactions

- Simplified operations management: Single dashboard for monitoring payments, unified reporting, consolidated vendor relationships

- Enhanced customer lifetime value: Consistent payment experience drives loyalty and repeat purchases across all touchpoints

- Reduced operational costs: Eliminated duplicate systems, streamlined reconciliation processes and unified compliance management

- Faster market expansion: Consistent payment infrastructure enables rapid deployment across new channels and geographies

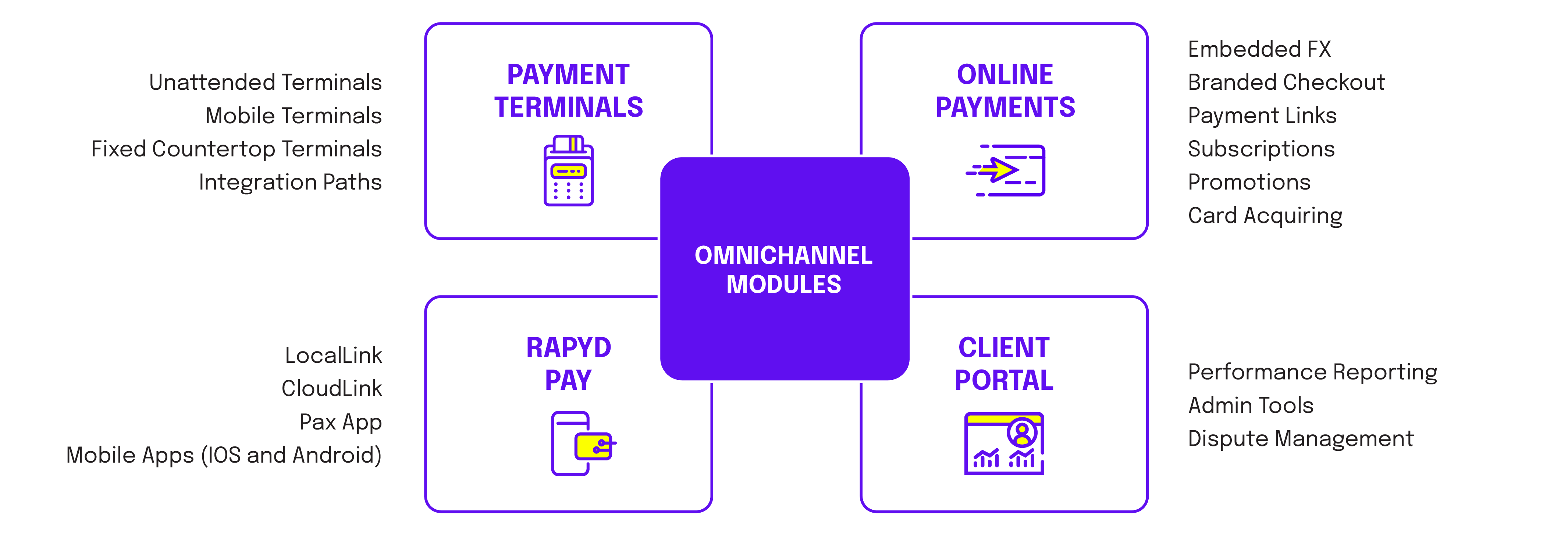

How Rapyd Accelerates Omnichannel Payments Success

You know the operational headaches that come from managing separate gateways, risk tools and reporting dashboards. Data gets duplicated, refunds take longer and each new channel requires another integration project.

Let’s explore how Rapyd eliminates these problems through four connected modules—online payments, payment terminals, Rapyd Pay and the Client Portal—delivered through one global infrastructure.

Each module connects to the same platform, giving you a single customer view, consistent fraud controls and shared settlement flows across all your markets.

Online Payments with Unified Vendor Management

Managing multiple payment providers creates unnecessary complexity. Different processors for web, mobile and recurring payments mean separate contracts, disconnected data and fragmented reconciliation. You spend time coordinating vendors instead of growing revenue.

Rapyd consolidates your payment infrastructure into one provider. Our platform handles card processing, alternative payment methods and digital wallets through a single integration. One API connects your website, mobile app and backend systems to more than 900 payment methods across 190+ countries.

Direct acquiring licences in the UK, Europe, Singapore and Israel means transactions reach card networks faster with fewer intermediaries. This unified approach reduces vendor management overhead whilst maintaining consistent performance across all digital channels.

Your developers work with one codebase, your finance team reconciles from one dashboard and your operations run smoother without juggling multiple provider relationships.

Payment Terminals for In-Person Transactions

Digital and physical channels often diverge the moment a card touches a countertop terminal. Rapyd bridges this gap with PAX smart devices and the Rapyd Apps, powered by the same acquiring stack that powers your website.

The refund logic stays synchronised because the terminal sends real-time events to your back end over the existing API. Contactless support, tap-to-phone and remote configuration provide modern in-store acceptance without separate vendor relationships.

Rapyd Pay for Flexible Payment Experiences

Rapyd Pay extends your payment capabilities beyond standard checkout flows. Generate payment links for invoicing, subscriptions or remote sales without building custom infrastructure. Share secure URLs via email, SMS or messaging apps and customers complete purchases from any device.

This flexibility supports diverse business models—marketplace vendors invoicing buyers, field sales teams collecting deposits or subscription services managing recurring billing. The same unified platform powers everything, maintaining consistent security controls and reporting across all payment types.

Client Portal for Centralised Management and Reporting

Running these payment systems only adds value when you can interpret the data. The Client Portal consolidates every transaction—whether card-present or card-not-present—into one dashboard. You track approval ratios by market, examine chargebacks, export settlement files and process refunds without switching between systems.

Centralised analytics reveal trends across channels, helping you identify localisation gaps or fraud patterns early and respond confidently. Finance teams can close books faster because reconciliation files share identifiers, currencies and fee structures.

Subscribe Via Email

Thank You!

You’ve Been Subscribed.