Examine key considerations for implementing recurring direct debit payments and the potential pros and cons

Are you weighing your options for collecting subscription payments from your customers? You might wonder how direct debit recurring payments compare to other methods. You might also want to address any concerns about fraud, failed payments, and refunds. This article will help you decide if direct debit recurring payments are right for you and your customers.

Direct Debit Recurring Payments: Why Consider Them?

You know the advantages of having reliable payment methods for your businesses subscriptions. You want to collect recurring transactions without fuss, keep your cash flow steady, and minimise disputes. Direct debit recurring payments let you accept or pull funds from a customer’s bank account. Once authorised, your system automatically collects the agreed payment amount from the customer’s bank account on specified dates.

This payment method works well for subscription services, gym memberships, utility bills, automated childcare billing and other recurring charges for physical and digital goods. You get more certainty about incoming funds, customers experience less hassle, and you can focus on giving them a better overall experience.

Recurring Card Payment vs Direct Debit: What’s the Difference?

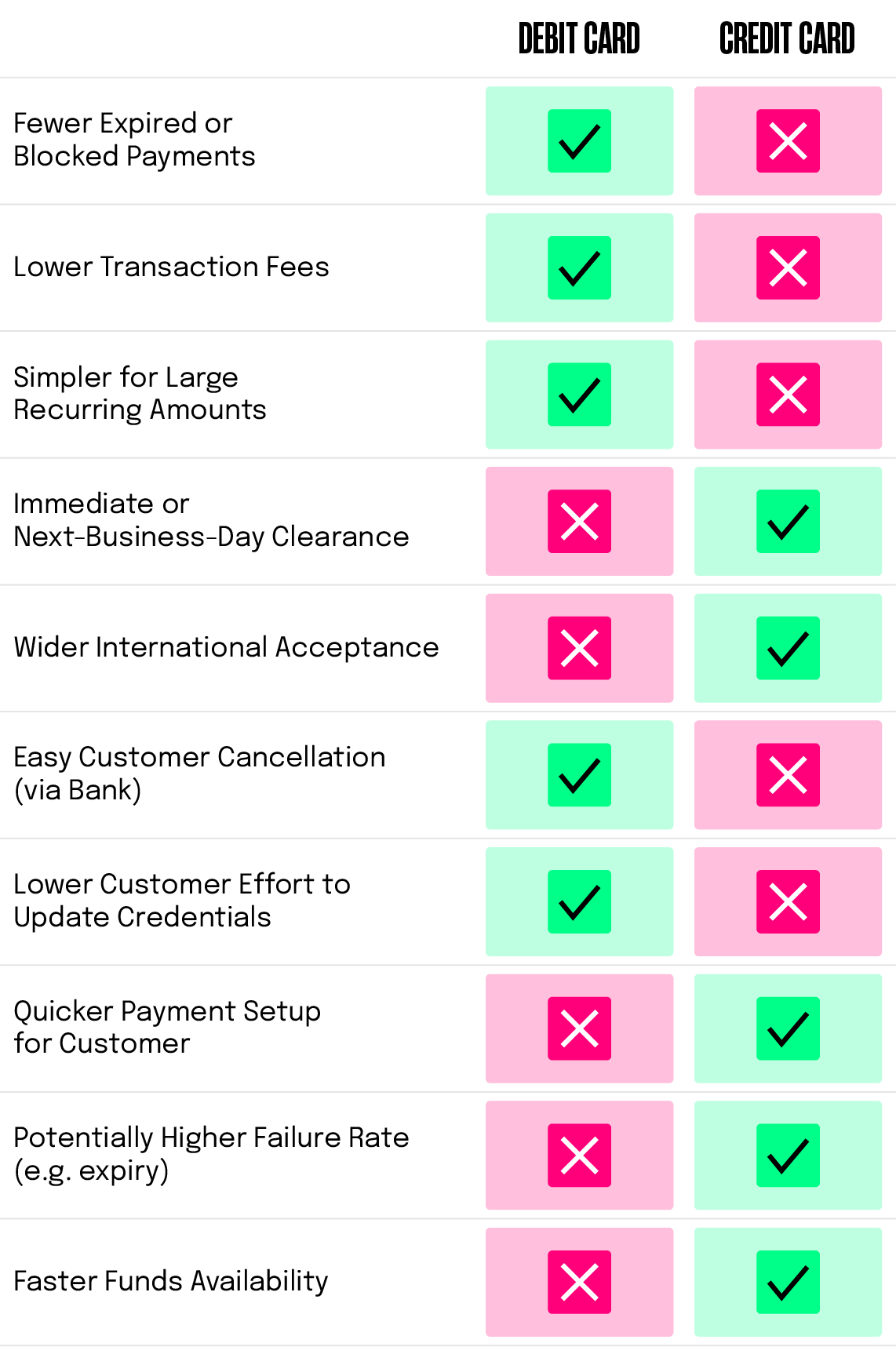

Recurring card payment methods rely on charging a debit or credit card at intervals set by you and your customer. They can clear faster than direct debit, but they often carry higher transaction fees. They might also pose a bigger risk of failed payments due to expired or blocked cards. You’ll probably need to manage card details and handle the times when customers cancel or replace their cards.

Direct debit recurring payments automatically collect funds from a customer’s bank account at agreed times. Bank accounts do not expire and rarely change. This difference often leads to lower failure rates. Direct debit typically offers simpler payment processing over the long term, though it can take a few extra days for funds to clear.

Comparison: Direct Debit VS Cards for Recurring Payments

Use this table to help you decide which recurring payment option(s) suits your service or product. Cards tend to be the go-to method due to greater convenience and adoption by consumers. However, direct debit can provide a valuable addition for some businesses.

Why Set Up Recurring Payments with Rapyd

With Rapyd, you can accept recurring card payments alongside alternative options like direct debit, giving your customers more choice and improving conversions. Rapyd’s platform lets you manage everything in one place. You can connect your billing tools through Rapyd’s API, automate collections and handle multiple payment methods globally. Whether you’re collecting monthly fees, subscriptions or invoices, Rapyd simplifies recurring payments for any industry.

Are Direct Debit Transactions Disputable?

Customers can review their statements to confirm each debit. If something isn’t correct, they can dispute it within the time limits set by local rules. For example, those using SEPA in the EU often provide an eight-week window for reversing direct debits on a “no-questions-asked” basis. While refunds might sound alarming, many businesses see few formal disputes if they maintain reliable records and timely communication with their customers.

Direct Debit Recurring Payments: Why Do Many Businesses Prefer This Payment Method?

- Lower Transaction Fee: Direct debit usually charges a small flat fee or a small percentage fee. This structure supports stable costs and can help large-volume merchants save money.

- Predictable Cash Flow: When you know exactly when your system collects payment, you can plan spending and manage your finances more effectively. Recurring payments give you the ability to keep an eye on your revenue without juggling guesswork around late or missed payments.

- Fewer Failures: A direct debit works with a customer’s bank details rather than a debit or credit card. Cards expire or get replaced more often. If a card expires, you’ll need to reach out for new details. The advantage of direct debit is that bank accounts rarely change, so you aren’t constantly chasing your customers to update credentials. This lowers your failure rates and can help you minimise payment friction.

- Reliable for Regular Payments: Subscription services and other recurring models do best when billing stays consistent. You don’t want to remind your customers each time a payment is due. With a direct debit, you set the schedule and your system automatically collects payment. This reduces the chance of friction and helps build better relationships with your customers.

- Protection from Disputes: Direct debit mandates require formal authorisation. When a transaction appears on the statement, your customer is more likely to recognise it and less likely to dispute it. While direct debit disputes can happen, they are often resolved when you supply the relevant mandate or proper record.

Potential Concerns About Direct Debit

- Fraud and Security: Businesses worry about unauthorised charges. However, direct debit solutions have systems that verify whether the bank account belongs to the named account holder. Banks also track suspicious activity. You might see fewer fraud cases with bank accounts.

- Chargebacks or Reversals: Customers can request a refund if they feel a charge was taken incorrectly. In certain regions, such as SEPA areas, you face an eight-week “no-questions-asked” refund period. As long as you keep a proper record of what your customers agreed to pay, you can contest improper reversals if local rules allow it.

- Integration and Setup You might wonder if your system can handle direct debit recurring payments. Many payment processing platforms offer APIs or plug-ins to help you create, manage, and track subscription payments. With an API, you can integrate payments with your billing or accounting tool to automate payment tracking. This helps you manage your entire payment cycle in one location.

Practical Uses: Who Benefits Most?

Direct debit recurring payments suit recurring costs, membership fees, monthly donations, and many subscription services. Some typical examples:

- Gym Memberships: Many gyms give customers a monthly direct debit option. This method helps the gym collect membership fees on time and reduces last-minute cancellations. Members avoid updating card details, and the gym sees fewer late or failed payments.

- Utility Bills: For variable usage such as electricity or water, you can use direct debit to collect amounts that differ each month. You inform the customer in advance, then collect the payment. You can handle changing rates or seasonal usage without requiring fresh payment authorisation.

- Professional Services: Consultancies and other B2B ventures sometimes issue monthly or quarterly invoices. Direct debit can ease the burden of chasing payments. Instead of waiting for each client to remember to pay, you collect funds on the due date, simplifying your cash flow management.

- Ongoing Subscriptions: Users who sign up for software-as-a-service or curated product deliveries often prefer a direct debit approach. They avoid repeated card entry and do not risk missing payments due to an expired card.

Standing Orders vs Direct Debit

A standing order also collects payment from a customer’s bank account, but it differs from direct debit recurring payments. With standing orders, the customer sets the amount and schedule, then instructs the bank to send those funds. You, as the business, cannot change the amount or frequency without the customer altering the instructions. Direct debit, by contrast, gives you more control to adjust the payment amount, notify the customer, and automatically collect it. This flexibility matters if you charge variable rates or often update your pricing.

Reducing Failed Payments and Improving Payment Conversion Rates

Even though direct debit typically has low failure rates, you may still deal with failed payments from insufficient funds. Some providers let you retry collecting the amount automatically after a set period, or you can arrange a manual retry policy. Since you know exactly when the payment cycle begins, you can alert customers about insufficient balance before the next collection. That transparency keeps them engaged and reduces friction.

Refining Your Process for Direct Debit Success

Use these tips to make the most of direct debit recurring payments.

- Clear Authorisation: Ensure your customers complete a valid debit mandate form. Explain payment amounts, intervals, and their rights to refunds. If they see a well-defined setup process, they trust that your business handles their information properly.

- Upfront Communication: Send a reminder before you collect direct debit payments. Inform your customers about changes in cost or schedule. This approach builds trust and reduces disputes.

- Automate Payment: Use a platform that integrates with your billing or accounting workflow. Align payment collection with your invoicing. Automation helps you reduce manual tasks and keep an eye on revenue.

- Track Transaction Fees and Overall Costs: Pay attention to each transaction fee or monthly charge if your provider has one. Keep an eye on total outgoings to see how much you save versus other methods.

- Plan for Cancellations and Refunds: You might want clear guidelines for how customers cancel their direct debit. Refunds can be less stressful if you prepare for them. Outline policies for partial refunds or missed deliveries if your subscription covers physical goods.

For Many Subscription Businesses, Direct Debit Recurring Payments Are a Valuable Addition to Their Payment Stack

Direct debit recurring payments help you focus on your business rather than chase late payments or replace out-of-date card details. They allow you to collect payment from a customer’s bank account without friction or guesswork. You get a predictable cash flow and reduced overall failure rates. If you run subscription services, memberships or handle frequent regular payments, direct debit might be the right fit.

Still unsure if it suits your model? Think about the reliability you gain and whether you’re comfortable with a few days’ clearance time. Direct debit recurring payments require a mandate and proper coordination, but once you set it up, you can reduce payment headaches and better serve your customers.

Grow Your Subscription Business with Rapyd

Simplify subscription payment processing with powerful features designed to maximise approvals and minimise churn.

Our solutions help businesses across industries, such as marketplaces, online gaming, financial services, pharma, and travel.

Subscribe Via Email

Thank You!

You’ve Been Subscribed.