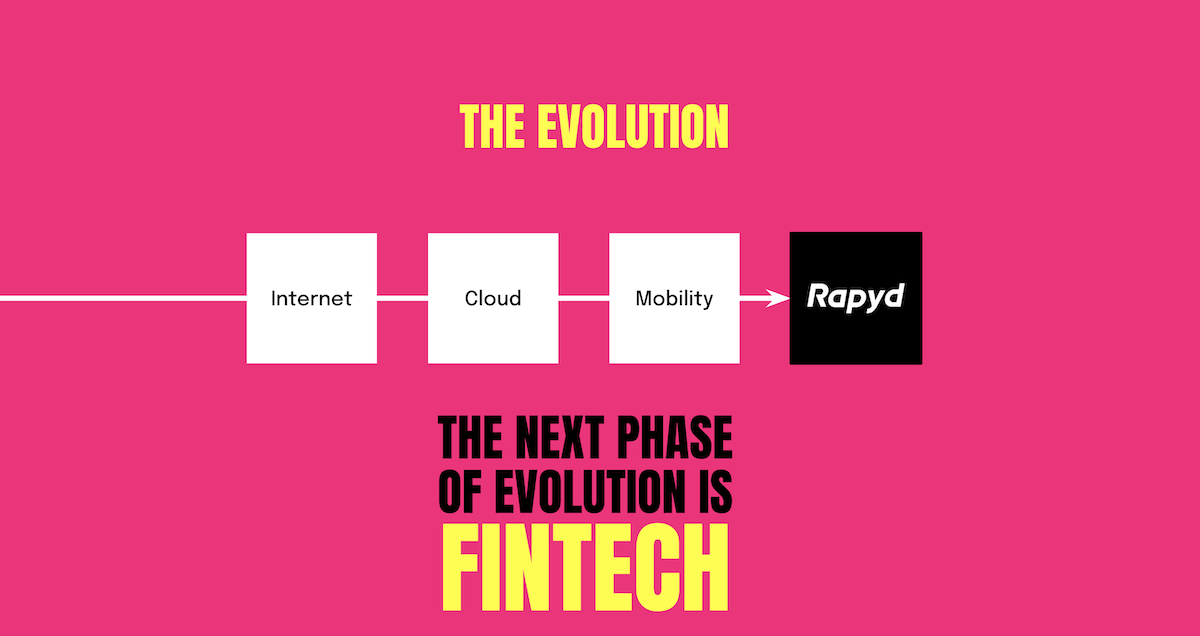

The Recipe to Make Money with Fintech

Embedded finance significantly increases the value you can provide customers. It helps customers stay inside your ecosystem. Keeping customers, not having churn and creating recurring revenue streams. Here’s the recipe to make money with software using financial services.

- You need to find a service that provides something basic that clients come in and do at a high frequency, that they come back again and again and again to use as the starting point of your recipe.

- Acquire users and collect data. Analyze the data to see what financial services your customers need and how you can deliver them better, faster, easier, or cheaper than the clerk behind his desk with a fax machine.

- Add financial services, wallet, credit, payments, bank transfer, whatever you want.

- Engage the users to create this repetitive model and you can upsell and cross-sell new services.

Case Study: How Shopify Turned Embedded Finance Into a Revenue-Generating Machine

Elon Musk says he wants to turn Twitter into the first super app for the West. I have bad news for Mr. Musk. It’s already been built. And it’s called Shopify.

Shopify is truly an unbelievable example. People know that if they want to build an ecommerce store, they go to Shopify. But Shopify is not an ecommerce company. Shopify is a fintech company.

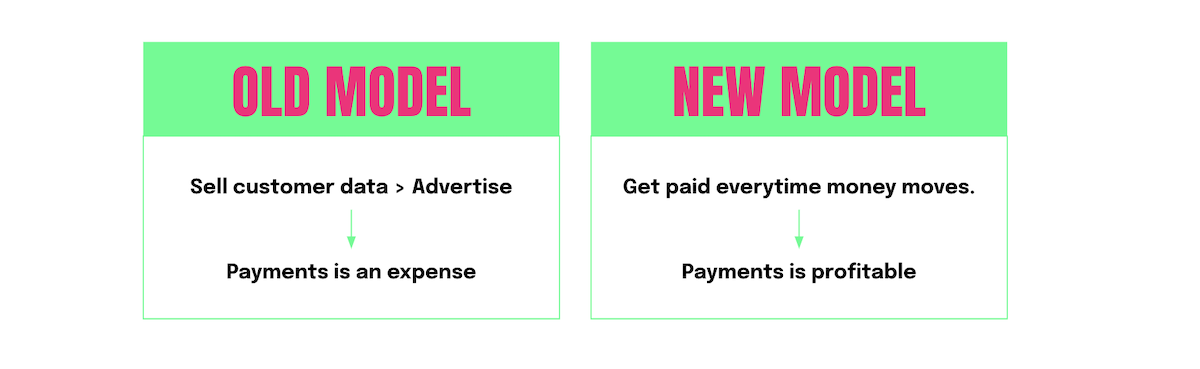

66% of Shopify’s revenue comes from embedded finance. They build a huge ecosystem around a basic offering of a website builder. They now have this offering of payments, business accounts, corporate cards and lending. If you look at Shopify today, their success has nothing to do with collecting $15 or $20 a month for a website. The payments and the fintech built into the Shopify offering is driving the majority of the revenue – and it’s continuing to grow up and up.

Shopify is redefining what a super app can be. It doesn’t have to be mobile. It doesn’t have to be a delivery service. It doesn’t have to be for consumers. It just needs to provide sticky financial services that are embedded seamlessly with other complimentary offerings.

As soon as you’re a Shopify client, and you’re using business accounts, payments and corporate cards, there is no way on planet Earth you will move to WooCommerce, or Wix or whatever. You’re going to stay inside this ecosystem. You might use some other companies for specific things, but Shopify is how you go to market.

More Embedded Finance Examples

Shopify is a great example, but it isn’t the only example. There are lots of companies that use embedded finance to generate revenue and reduce customer churn.

There are messaging applications. For example, Facebook and WhatsApp are doing WhatsApp Pay, and you have Alipay and you have WeChat, and Viber is now doing Viber Payments.

You have social media, gaming companies and logistics and transportation. For example, Uber, Grab, Gojek, and DiDi. It’s harder to list a mobility app that isn’t a fintech. They’re making money from embedded finance by offering an endless number of financial services to their drivers and their consumers. Imagine telling Microsoft in the 2000s that you could be making money off customers and workers. Bill Gates’ head would have exploded.

Even ecommerce companies are making money by offering either corporate cards, virtual cards or loyalty cards. They offer their seller protection, buyer protection, lending, business bank accounts and an endless number of offerings, and it’s not even their core businesses.

Once you are handling money for a user, you can build a castle of services within your platform. – Sidu Ponnappa, Gojek

Find Your Inner Fintech

Rapyd is a developer-driven company. I encourage you to start building. Because at the end of the day, that’s the reason why you’re reading this – to build better tools that help you and your customers live your dreams.

The first step is to reach out to our Partnership Team and learn more about our Partnership Program.

If you are a developer, we have a community that you need to join, community.rapyd.net.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}