A quick refresher: what are stablecoins used for?

Stablecoins are a type of cryptocurrency designed to hold a steady value against a reference asset, usually the US dollar or short-dated US Treasuries. Because they don’t swing in price the way bitcoin or ether do, they can serve as a more practical settlement asset, a store of value or a medium of exchange.

Common stablecoin use cases include:

- Trading and providing liquidity across crypto exchanges and DeFi protocols

- Cross-border payments and remittances

- Business-to-business supplier payments

- Payroll and contractor payouts

- Corporate treasury management and internal transfers

- Holding dollar-denominated value in countries with currency instability

The four largest stablecoins — USDT, USDC, USDE and USDS — account for more than 90% of total supply, making them a reasonable proxy for what’s happening across the wider market.

How are stablecoins used in practice? Four functional categories

The Kansas City Fed analysis groups stablecoin holdings into four broad functions. Together they show where the money sits and what it’s doing.

Trading assets cover stablecoins moving inside the crypto financial system. They provide liquidity to centralised and decentralised exchanges, act as collateral in DeFi lending and borrowing, and let traders park capital between trades without converting back to fiat. This category also includes stablecoins held inside infrastructure protocols, mostly bridges that move value between different blockchains.

Payments are stablecoins used to settle real-world transactions: peer-to-peer transfers, cross-border remittances, consumer-to-business purchases, B2B supplier payments and B2C flows like payroll.

Transfers capture high-value movements that aren’t strictly payments. These include corporate treasury flows between subsidiaries, money moving in and out of crypto finance, and settlement legs for tokenised assets.

Idle holdings refer to stablecoins sitting in wallets that rarely move — sometimes lost, sometimes forgotten, sometimes used as informal dollar savings accounts.

The actual distribution: where stablecoins live

Using data from DeFiLlama’s stablecoins tracker alongside payment volume figures and earlier research from Forbes, the briefing estimates how stablecoins are split across these functions as of late 2025.

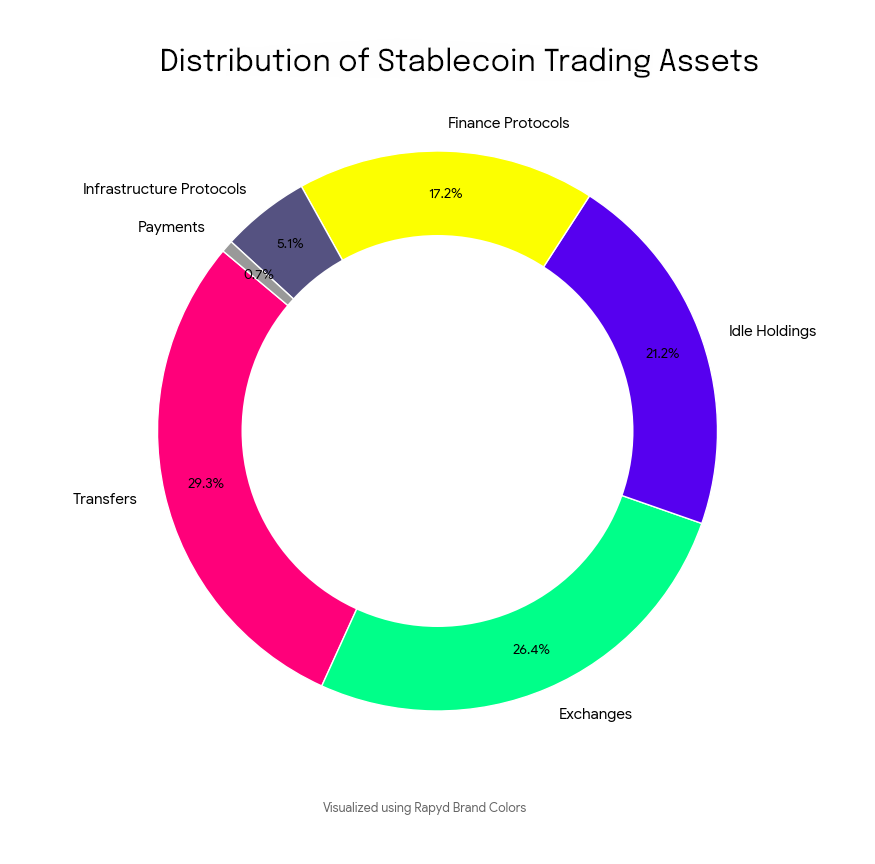

Trading assets account for roughly 48.8% of all stablecoins in circulation. Within that, exchanges hold about 26.4%, finance protocols hold 17.2% and infrastructure protocols hold 5.1%. Transfers make up around 29.3%. Idle holdings sit at about 21.2%. And payments account for 0.7%.

Why use stablecoins for payments? The promise vs the data

The case for using stablecoins instead of fiat is well understood. They settle in seconds rather than days. They operate 24/7. They don’t rely on the chain of correspondent banks that makes traditional cross-border payments slow and expensive. They don’t incur interchange fees or subject businesses to chargeback risk. For businesses, those advantages are significant.

So why are stablecoin payments still less than 1% of total stablecoin use?

More than 5% of all stablecoins are tied up in bridges and other infrastructure protocols whose entire purpose is moving tokens between blockchains. That tells you the ecosystem still lacks proper interoperability — value can’t yet flow freely across chains or a single dominant chain hasn’t emerged for transactions.

Acceptance is uneven. Even with consumer wallets and merchant integrations growing, the network of places that actually accept stablecoins for goods still lags cards.

Crypto finance (difi) still dominates. Nearly half of all stablecoins are being used inside the crypto financial system. Even so, stablecoin payments are growing after the GENIUS Act passed in July 2025.

Why use stablecoins instead of USD or local fiat?

For everyday payments inside developed markets with strong banking infrastructure, the answer is often that you currently don’t.

But a strong case for stablecoins shows up in other scenarios:

- Cross-border B2B payments where traditional rails take days and pass through multiple intermediaries

- Payouts to contractors, sellers or workers in markets with limited banking access

- Treasury movements that need to happen outside banking hours

- Holding dollar-denominated value in economies with high inflation or capital controls

- Settling tokenised assets where the cash leg needs to live on the same ledger

- Eliminating the need for prefunding and freeing up working capital

- Agentic commerce

These are the use cases driving real adoption today, particularly among financial institutions, marketplaces and businesses with global operations.

The interoperability problem holding stablecoins back

One of the more striking findings in the briefing is how much stablecoin supply is currently locked inside infrastructure protocols that move stablecoins from one blockchain to another. Smart contracts lock tokens on one chain while minting equivalent tokens on another.

The fact that this needs to happen at all, and that more than 5% of total supply is committed to it, points to a limitation of stablecoins that function across blockchains. Stablecoins were meant to function like programmable digital cash, but the digital cash on Ethereum doesn’t natively talk to the digital cash on Solana or Tron. Until that changes, a meaningful share of the ecosystem’s resources will keep going to infrastructure rather than to payments or transfers.

What this means for businesses considering stablecoin payments

If you’re a business weighing whether to accept or send stablecoins, the data offers useful insights. Stablecoins are a powerful tool for specific workflows, such as cross-border B2B payments, treasury management and payouts. They aren’t yet a general-purpose payment method that competes with cards or local rails for everyday consumer transactions.

The smart approach is to identify the workflows where stablecoins genuinely solve a problem you have today, run controlled pilots with proper compliance and reporting, and build from there. Treat stablecoins as another rail in your payments stack rather than a wholesale replacement for what you already use.

{kind=link}